Europe Wealth Paths for Data Professionals

Employee, contractor, special tax regimes, or digital nomad — how an immigrant in Europe builds multiple income streams and keeps more of them.

In Part 1 (Canada) the biggest lever on your take-home was your income structure — employee vs corporation. In Part 2 (USA) it was your state — Texas vs California. In Europe the lever is bigger than both: it is the country itself. Tax systems differ wildly between neighbours, and — here is the key idea of this post — the immigrant is the only person who gets to choose one.

Locals are stuck with their system. A newcomer can pick where to land, and half of Europe runs special tax regimes designed exactly for newcomers: flat 20–24% rates, 50% exemptions, decade-long windows. This post maps how a data professional in Europe gets paid — employment, stock, contracting, your own company, digital nomad visas — and how an immigrant combines them into the ideal setup: a stable anchor, multiple income streams, and the lowest legal tax.

A note on roles. For simplicity, I use the role of data engineer throughout. But it doesn’t matter — the same map applies to data analysts, analytics engineers, BI developers, software engineers, product managers, and more. What changes your take-home is the structure of your income, not your job title.

Not tax advice. This post is general information for learning. All numbers are for the 2025–2026 tax years and change often — several changed while this post was being written. Rules differ by country, region, and personal situation. Before you act, talk to a local tax adviser (and for anything cross-border, a cross-border one). A good adviser costs less than one mistake.

Part 1 — The default: employment in Europe (and why your payslip looks different)

Everywhere in Europe, the default is the same as in North America: you are an employee, one company pays you a salary, and tax comes off the top before you see it. What is different is how much comes off — and what you get back.

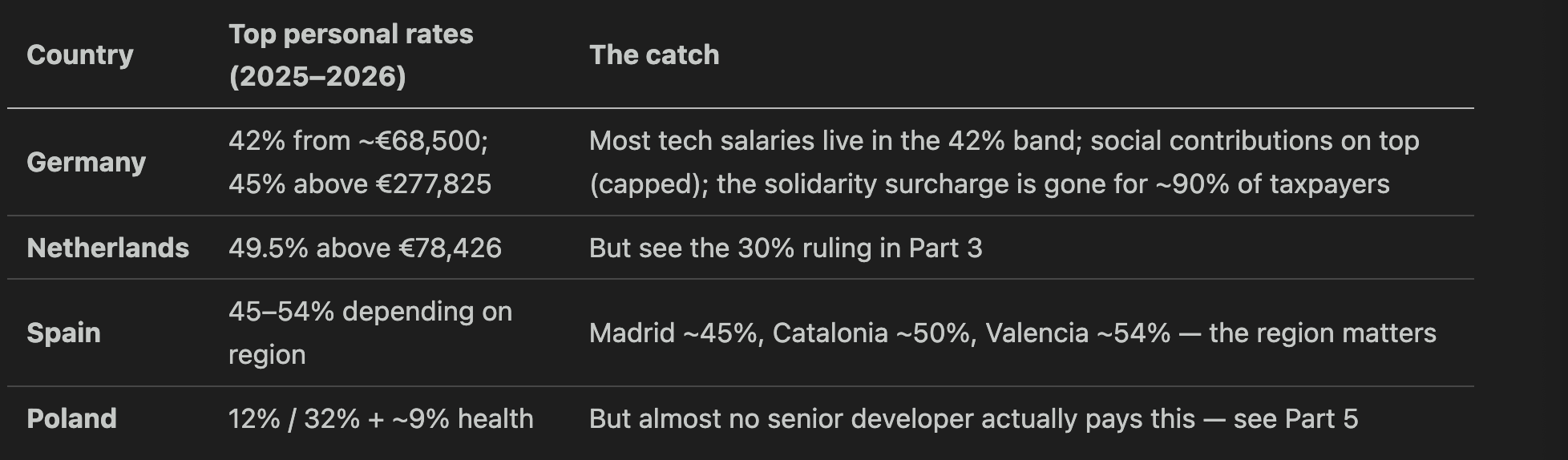

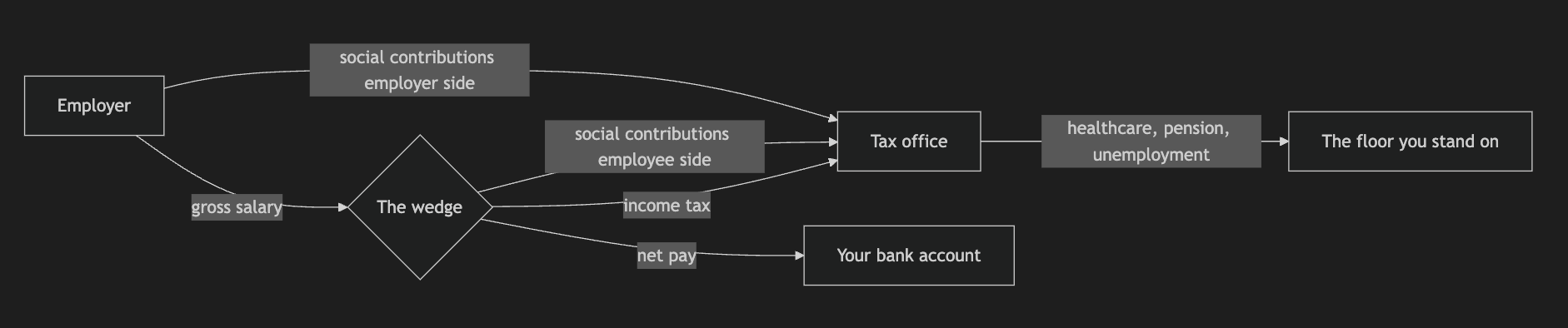

The number to know is the tax wedge: income tax plus social contributions, paid on both the employee and the employer side. In much of Western Europe, the total wedge on a senior salary runs 40–50%+. A few verified examples:

Before you close the tab: you get more back than in North America. Public healthcare with no employer-plan anxiety. Real pension accrual. Labor protections, notice periods, severance. 25–30 days of actual vacation. The European deal is a higher wedge and a higher floor. Whether that trade is good depends on what you are optimizing — this post is about keeping the floor while lowering the wedge.

The immigration anchor: the job IS the visa

Here is the part North American readers never have to think about. For most immigrants in Europe, the job is not just income — it is legal status.

The main work-immigration tool is the EU Blue Card: a residence permit for skilled workers with a job offer above a salary threshold. In Germany for 2026 that is €50,700 gross (general) or €45,934 for shortage occupations — and IT is a shortage occupation; experienced IT specialists can even qualify without a university degree (3+ years of relevant experience). The Blue Card is also the fastest road to permanence: in Germany, permanent residency after 27 months — or just 21 months with B1 German (plus pension contributions throughout).

The implication shapes everything in this post: quitting your job to contract full-time is not just a financial decision in Europe. Until you hold permanent residency, it can be an immigration decision. Keep that in mind every time a later section makes contracting look attractive.

Key takeaways — Part 1

Europe’s tax wedge (income tax + social contributions) runs 40–50%+ — higher than North America, but it buys healthcare, pension, and real vacation.

Rates vary hugely by country — and inside Spain, by region.

For immigrants, the EU Blue Card job is the visa and the fastest PR track (Germany: 21–27 months).

Until you have permanent residency, income decisions are also immigration decisions.

Part 2 — Stock compensation: RSUs in Europe

Big-tech offers in Dublin, Amsterdam, Berlin, or Madrid come with RSUs, exactly like Seattle. The mechanics are the ones from Parts 1–2: shares vest on a schedule, the value at vesting is employment income, sell-to-cover takes a chunk, and growth after vesting is a capital gain.

The European twist: at vesting, RSUs often attract not only income tax at your marginal rate (45–55% in much of Western Europe) but social contributions too, so the total haircut can exceed the North American one.

Reliefs exist, but they are narrow and local:

France has a qualified regime for free shares (”Macron” plans): the acquisition gain up to €300,000/year is taxed only at sale, with a 50% rebate — roughly 38% effective. But it requires the employer to run a French-qualified sub-plan.

Spain exempts €12,000/year of employee shares — but only if the plan is offered to all employees on equal terms, which typical selective tech RSU grants are not. Certified startups get a better deal (€50,000 with tax deferral).

The rule: ask locally, never assume. The same Amazon grant is taxed three different ways in three neighbouring countries.

Key takeaways — Part 2

RSUs vest as employment income, often plus social contributions — the haircut can beat North America’s.

Qualified-plan reliefs exist (France’s Macron regime) but are narrow; Spain’s €12k exemption rarely fits selective tech grants.

Same grant, different country, different tax — check locally.

Part 3 — The immigrant superpower: special inbound tax regimes ⭐

Now the heart of the post. Remember the wedge from Part 1? Half of Europe will cut it dramatically — but only for newcomers.

These are inbound tax regimes: multi-year tax discounts for people who move in, designed to attract exactly the reader of this post — skilled professionals with mobile income. Locals cannot have them. Returning citizens usually cannot have them (lookback rules). A newly arrived data engineer can.

Here is the verified 2025–2026 map:

Look at what this does to Part 1’s table. The Netherlands’ scary 49.5% becomes ~35% effective under the 30% ruling. Spain’s 45–54% becomes a flat 24%. Portugal’s progressive scale becomes 20%. Same job, same city, same desk — a newcomer keeps tens of thousands more per year than the local sitting next to them.

The counter-example: Germany

And now the country the most immigrants actually move to. Germany has no inbound regime. None. A 2024 proposal to give newcomers a 30/20/10% rebate over three years was never legislated — it died with the government that proposed it and is absent from the current coalition’s plans. Germany offers excellent salaries, the Blue Card, and the full 42% + social contributions from day one. Great jobs, zero tax welcome mat. (France has a regime — up to 8 years — but only for employees recruited from abroad by a French company. Move first, job-hunt later, and you are not eligible.)

Play the window

Every regime above is time-boxed: 5, 6, 7, 10, or 17 years. The strategic consequence: realize your highest income inside the window. Take the big-RSU job, push for the promotion, land the fat contracts during the regime years. The discount is temporary — treat it like one.

⚠️ Regime risk is real. Conditions are strict (non-resident lookbacks of 3–15 years, qualifying professions or employers, minimum stays with clawback). And regimes change with politics: Portugal already killed the original NHR for new entrants in 2024, and the Netherlands trimmed 30% to 27% starting 2027. Get in correctly (deadlines matter — Spain gives you 6 months, Portugal a hard January 15), and never build a 10-year plan on a regime surviving 10 years.

Key takeaways — Part 3

Half of Europe offers newcomer-only tax discounts: Spain 24% flat, Portugal 20% flat, Italy 50% off, NL ~30% tax-free slice, Cyprus 0% dividends.

Germany has none — full freight from day one.

Regimes are time-boxed — front-load your peak earnings into the window.

Deadlines and lookback rules are strict; apply correctly or lose it.

Part 4 — Digital nomad visas: who has them, what they actually give

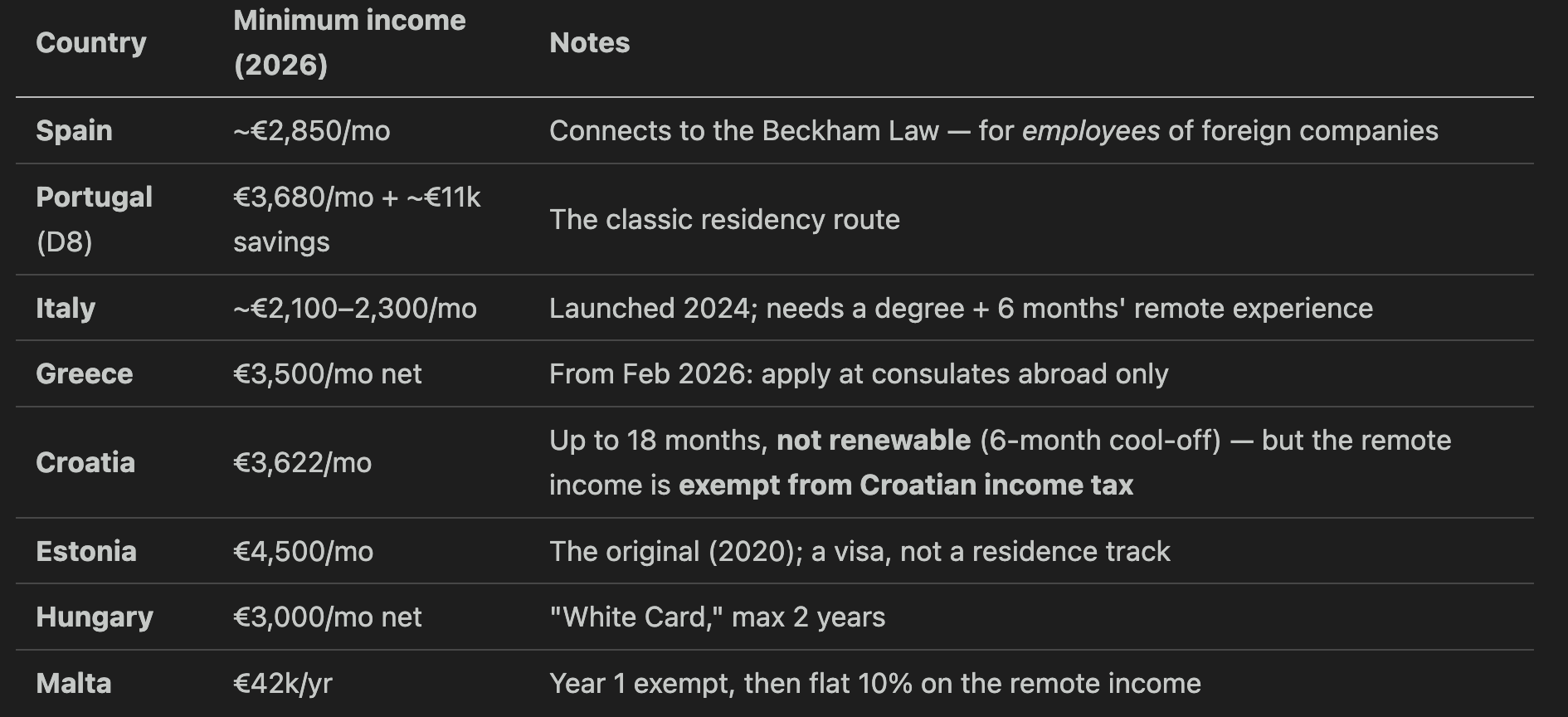

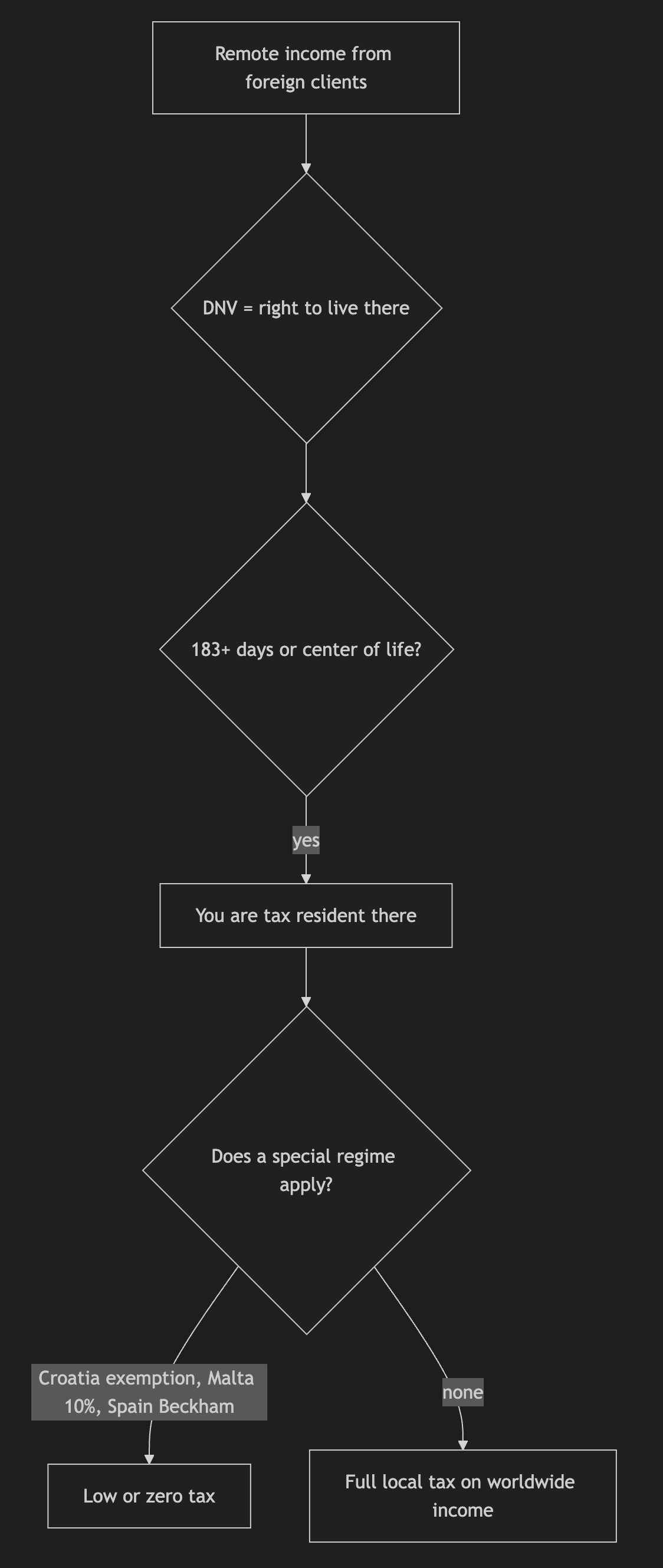

A digital nomad visa (DNV) is a residence permit for people who work remotely for foreign clients or employers. It answers one question only: may I legally live here while earning from abroad? It is not automatically a tax deal — hold that thought.

Who has one, verified with 2026 income thresholds:

Who does not: Germany — no DNV. The closest thing is the freelancer (Freiberufler) permit: discretionary, slow, and authorities like to see German clients — a pure remote worker with US clients fits it poorly. Austria has none either. The pattern from Part 3 repeats: the countries that court mobile talent are in the south; the biggest economy does not.

A visa is not a tax address

The confusion to kill: a DNV does not decide where you pay tax. Tax residency follows the 183-day rule and your center of vital interests (home, family, economic ties). Live somewhere most of the year and it is your tax home, DNV or not. A few DNVs do attach real tax treatment — Croatia’s exemption, Malta’s 10%, Spain’s bridge into Beckham — but that is the tax law of that country, not a property of nomad visas in general.

The clock changed: Portugal

One verified update that outdates half the internet’s advice: Portugal’s citizenship timeline moved from 5 years to 10 (7 for citizens of Portuguese-speaking countries) under a law in force since May 2026, with language and civics tests added. Applications filed before 19 May 2026 keep the old 5-year rules. If your plan was “D8, five years, EU passport” — that plan now takes a decade. Plan accordingly.

The honest caveat on nomadism. Hopping DNVs every 12–18 months means no permanent-residency clock running anywhere, no pension accruing anywhere, and a tax-residency picture that gets murkier every move. Nomadism is a great phase. It is not a structure. At some point the ideal setup needs an anchor — which is where the next parts go.

Key takeaways — Part 4

DNVs exist in Spain, Portugal, Italy, Greece, Croatia, Estonia, Hungary, Malta (~€2,100–4,500/mo income required). Germany and Austria have none.

Visa ≠ tax. The 183-day rule and your center of life decide where you owe.

Croatia and Malta attach real tax breaks; Spain’s DNV bridges into the Beckham Law for employees.

Portugal’s citizenship path is now 10 years, not 5.

Nomadism is a phase, not a structure — eventually you want an anchor.

Part 5 — Going independent: sole trader, B2B culture, and your own company

Now the contracting layer. Every European country has a sole trader / self-employed status (autónomo in Spain, Freiberufler in Germany, ENI in Portugal, JDG in Poland). What most people miss is that several countries run simplified regimes for the self-employed that are quietly excellent — and one country turned contracting into the national default for tech.

Poland: the B2B nation

The flagship example. In Polish tech, roughly 60–65% of senior developers do not have jobs — they have B2B contracts. Job boards like justjoin.it and nofluffjobs list two salary ranges per posting: employment (UoP) and B2B. The B2B one is 13–26% higher.

Why: a self-employed IT professional in Poland can elect ryczałt — a lump-sum tax of 12% of revenue for software services (no expense tracking, no 32% bracket), plus a fixed-tier health contribution. Compare 12% flat against the 32%+9% a senior employee pays at the margin, and the entire market’s behavior makes sense. (An 8.5% rate exists for some IT services, but tax authorities contest it for software work — get a private ruling before relying on it. And you cannot bill your ex-employer for the same work you did as an employee.)

Other simplified regimes worth knowing

Portugal (simplified regime): only 75% of services income is taxable, up to €200k revenue. Below ~€30k gross, genuinely zero expense tracking; above that, a 15%-of-income slice must be justified by expenses or an allowance.

Czech Republic (paušální daň): one flat monthly payment (~10,000 CZK in band 1 for 2026) covers income tax, social, and health for revenue up to ~1.5M CZK. The simplest tax life in Europe.

Romania: 10% flat personal income tax; the famous micro-company regime still exists but was tightened hard — 1% revenue tax, capped at €100k (2026) and one employee required.

Bulgaria: 10% flat personal and corporate tax, and freelancers deduct 25% of income as statutory expenses — ~7.5% effective before social contributions.

Your own company — and the trap everyone walks into

The next step up is a company: a local Ltd/GmbH/SL — or the internet’s favorite, an Estonian OÜ via e-Residency. Estonia charges 0% corporate tax on retained profits; tax (22%) hits only when you distribute. Run lean, reinvest, defer — it is the Canadian-corporation logic from Part 1 with a European passport. (Verified: the rumored extra profit taxes for 2026 were repealed before ever taking effect; the 0%-until-distribution system stands.)

⚠️ The trap of the whole post: you cannot live in Berlin with an Estonian company.

Here is the fantasy: live wherever you like, run everything through a 0%-tax Estonian OÜ, pay nothing locally. It does not work, and it fails on a rule every developed country has: place of effective management. If you sit in Germany and make the company’s decisions from Germany, the company is German-tax-resident — German corporate tax, German filings, the whole apparatus. CFC rules can catch what that misses.

Do not take my word for it — take Estonia’s. The e-Residency program’s own official guidance says: “E-Residency does not exempt companies from dual tax residency or foreign tax liabilities” — and its own worked example of an e-resident working from Germany concludes the profits are taxable in Germany.

e-Residency is a genuinely great admin tool: EU company, clean banking, all online. It is not a tax address. Your company is taxed where you run it — which means the real move is choosing where you sit (Part 3), not where the company is registered. This is Europe’s cousin of Canada’s PSB trap: the structure does not survive contact with substance.

Misclassification, Europe edition

Contracting full-time for one client looks like employment, and Europe polices that line harder than North America:

Germany — Scheinselbständigkeit (”fake self-employment”): the pension authority runs status determinations; the client owes up to 4 years of back social contributions (30 if intentional), with criminal exposure for the client’s managers. German companies are therefore deeply cautious about single-client freelancers.

Netherlands — the DBA rules: enforcement resumed January 2025, default fines from 2027. Dutch clients are re-papering contractor relationships right now.

Spain — falso autónomo: €3,750–€12,000 fine per misclassified worker plus back contributions.

UK — IR35: the client determines your status and carries the liability.

The tests are the same everywhere, and the same as in Parts 1–2: who controls the work, whose equipment, how many clients, who carries business risk. The practical effect on you: look genuinely independent or watch clients push you into payroll or agency arrangements at worse rates.

VAT in two paragraphs

Once your revenue passes the national threshold (Germany €25k, Poland ~PLN 240k, varies), you register for VAT. Sounds scary; for a B2B tech contractor it mostly is not:

Invoices to business clients in another EU country carry 0% VAT under the reverse charge — the client self-accounts for it; you just need a validated VAT number and a recurring sales listing. Invoices to US clients are outside EU VAT entirely. The paperwork is real but mechanical — this is what your accountant is for.

Key takeaways — Part 5

Simplified regimes are Europe’s hidden gem: Poland 12% ryczałt (the B2B nation), Portugal’s 75% rule, Czech flat tax, Bulgaria ~7.5% effective.

An Estonian OÜ is 0% until distribution — but is taxed where you actually run it. e-Residency itself says so. Choose where you sit first.

Misclassification enforcement is fierce (Germany’s Scheinselbständigkeit, NL’s DBA since 2025) — stay genuinely independent.

Reverse charge makes EU B2B invoicing 0%-VAT; US clients are outside VAT scope.

Part 6 — Cross-border: EU mechanics + earning USD from Europe

The EU hands you two mechanics that make multi-country income dramatically simpler than anywhere else:

One social security at a time. Under EU rules you contribute in exactly one member state, whatever mix of countries you work across; the A1 certificate proves which. No double CPP/FICA-style problems inside the EU.

Frictionless B2B. The reverse charge from Part 5 means a contractor in Kraków can invoice a client in Amsterdam as easily as one across the street.

And then there is the dollar. The same Deel / Remote.com / EOR machinery from Parts 1 and 2 works from Europe: a US startup pays you as a contractor, you file a W-8BEN(-E), US withholding drops to ~0%, and you are taxed where you live.

Note how the currency angle reverses versus Canada. A Canadian pockets the exchange rate (USD ~1.40 CAD). A European’s win is different: US-level rates at European costs. A $120/hour US contract is ordinary in Seattle. Earned from Valencia, Kraków, or Lisbon — cities where a nice life costs a third of the Bay Area — it is wealth-building money. Stack it with a Part 3 regime (that contract income at Portugal’s 20% flat, or through Poland’s 12% ryczałt) and you have the arbitrage this whole series is about.

Key takeaways — Part 6

A1 certificate: one social security system at a time, EU-wide.

US clients pay via Deel-type platforms with ~0% US withholding (W-8BEN); you are taxed where you live.

The European arbitrage: US rates × European costs × a newcomer tax regime.

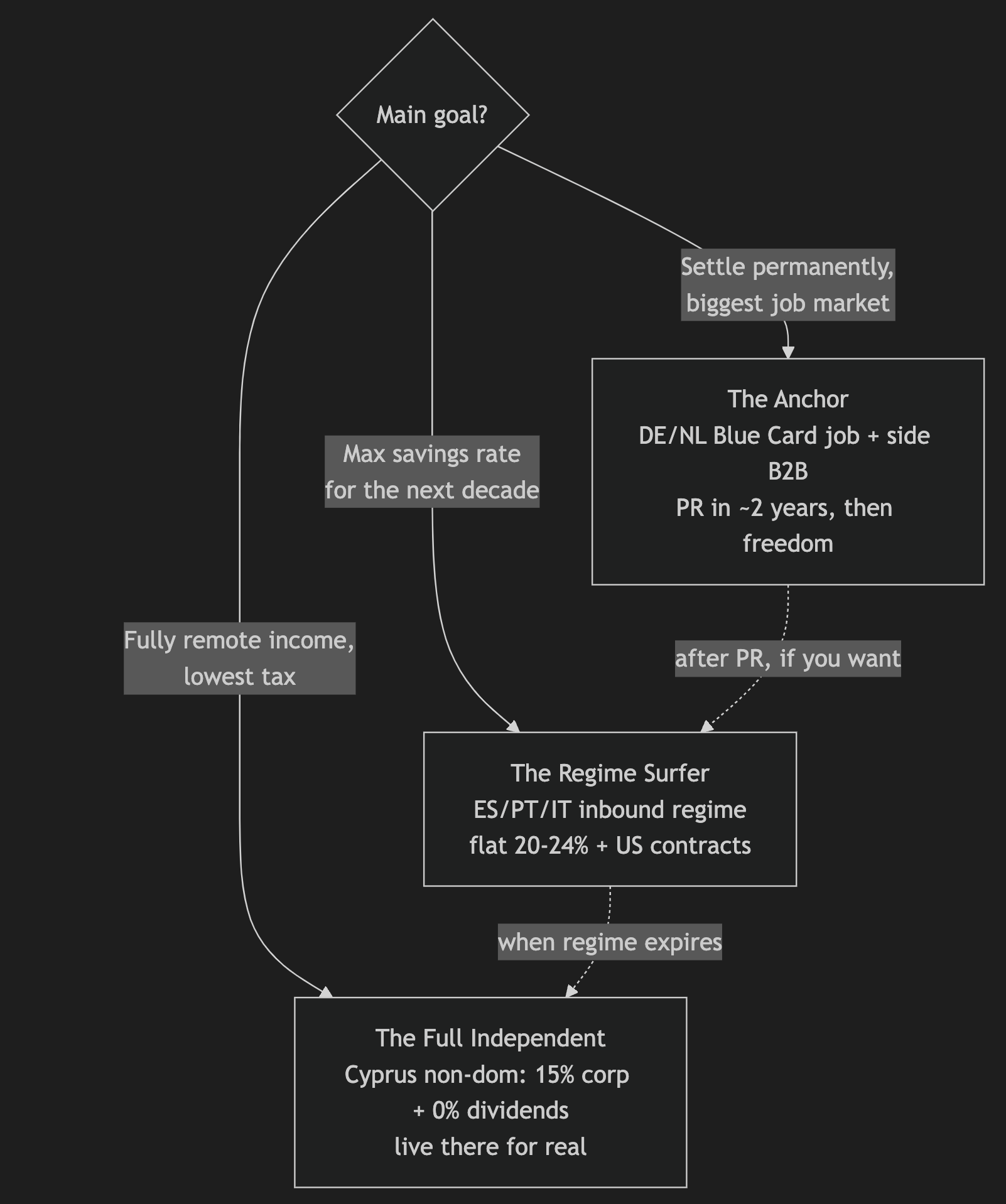

Part 7 — The ideal immigrant setup: job + side income streams

Now assemble it. The reader of this post wants three things at once: multiple income sources (because layoffs), low tax (because the wedge), and safe immigration status (because everything else depends on it). No single choice gives all three — combinations do.

First: are you even allowed to moonlight?

In North America this is a contract question. In Europe it is a permit question, and the answer varies (verified):

Germany (Blue Card): side self-employment needs prior permission from the immigration office — discretionary, city-dependent (Berlin grants it readily; Munich and Hamburg want a formal application before you invoice anything).

Netherlands: permissive — Blue Card / highly-skilled migrants may freelance on the side as long as the main job and its salary threshold stay intact.

Spain: since the 2025 immigration reform, an employee work authorization generally covers self-employment too.

Plus the ordinary layer: employment contracts in Germany and the Netherlands commonly require notifying (or getting consent from) your employer for side work. The rule: check the permit AND the contract before the first invoice. After permanent residency, all of this evaporates — one more reason the PR clock matters.

A quiet financial bonus of job-plus-side over pure contracting: your employment usually already covers your social contributions, so side income often adds only income tax — the expensive part of self-employment is already paid.

The three archetypes

Every sensible setup I have seen is a variation of one of these:

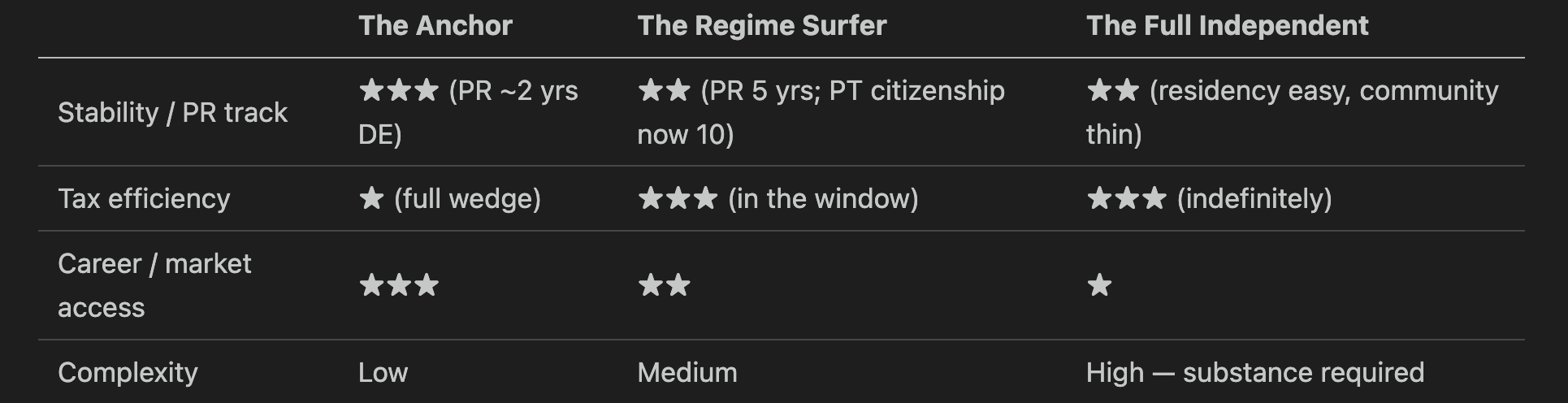

1. The Anchor — Blue Card job in Germany or the Netherlands + side B2B contracts. Maximum stability and the fastest permanent residency in Europe (Germany: 21–27 months). Taxes are high and the side gig needs permission in Germany — but after PR you are free, in the continent’s biggest job market, with the side business already warm. Best when long-term settlement is the goal.

2. The Regime Surfer — move to Spain, Portugal, or Italy on a job or DNV, stack the inbound regime, contract for US and EU clients. The best income-to-tax ratio in Europe for the regime’s window: a flat 20–24% on strong income, US contracts at European costs, sunshine included. The clock runs (5–10 years), citizenship in Portugal now takes 10, and the regime’s conditions must be maintained. Best when maximizing the next decade’s savings rate is the goal.

3. The Full Independent — base in Cyprus (or genuinely live in Estonia) and run everything through your company. Cyprus: 15% corporate tax (from 2026, still among Europe’s lowest), and as a non-dom, 0% tax on dividends for 17 years — a contractor billing through a Cypriot company and paying themselves dividends keeps more than almost anywhere else on the continent. The price: you must actually live there (Part 5’s trap — substance is everything), far from the big tech hubs. Best when income is fully remote and tax is the top priority.

And the closing philosophy of this series, with the European sharpening: job security is a myth — and here, your visa may depend on the job. A layoff in month 18 of a Blue Card is an immigration event, not just a financial one. So build the second income stream before you need it, inside your permit’s rules, and run the PR clock down as fast as the language courses allow. The job pays for your life; the side income builds your independence; permanent residency makes both of them optional.

Key takeaways — Part 7

Check permit + contract before moonlighting: Germany needs prior permission; NL is permissive; Spain allows it since 2025.

Job + side income often means social contributions are already covered — side euros are cheap euros.

Three archetypes: Anchor (DE/NL job + side B2B → fast PR), Regime Surfer (ES/PT/IT flat-tax window), Full Independent (Cyprus non-dom).

Your visa depends on the job — build income #2 before you need it.

Part 8 — Make the money work: accounts, pensions, and the exit-tax trap

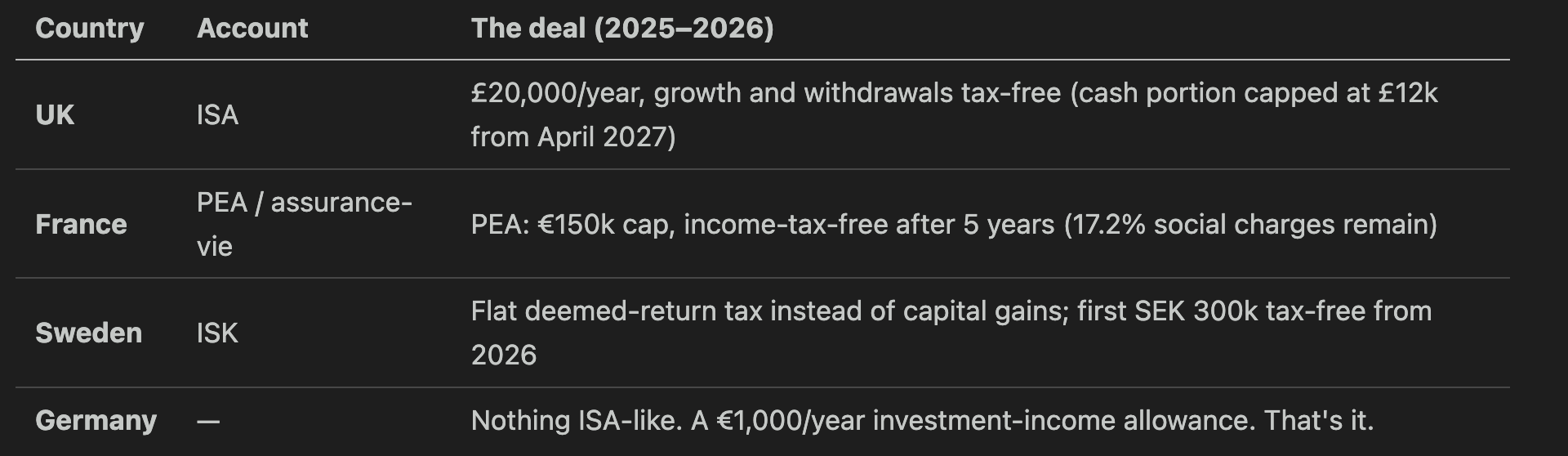

The Canadian and US posts ended with the TFSA/Roth playbook. Europe needs a different warning first: there is no pan-European tax-free account. Tax-advantaged investing is national, and it does not move with you:

Move from London to Berlin and your ISA’s tax-free status means nothing to the Finanzamt. The rule for mobile professionals: know your country’s wrapper, use it while you are there, and never assume it travels. (The EU floated a recommendation in 2025 nudging members toward ISA-style accounts — watch that space, expect nothing soon.)

Pensions: the European three-pillar systems often include an employer-matched occupational pillar — mandatory in Switzerland, near-universal in the Netherlands. The 401(k) rule from Part 2 of this series applies unchanged: matched money is free money; take all of it.

The exit tax: the dark twin of regime-surfing

This whole post celebrates mobility. Here is what mobility costs if you plan it badly: leaving a country can itself be a taxable event.

Germany (Wegzugssteuer): own ≥1% of any corporation — including your own GmbH or that Estonian OÜ — and moving your tax residence out triggers a deemed sale of the shares, tax due on paper gains. Since 2025 it also catches large fund/ETF positions (≥€500k invested per fund).

France: exit tax on portfolios above €800k (relief if you hold on for years after leaving). Spain: above €4M, or €1M with a 25% stake. Norway: latent gains above ~NOK 3M, now payable within 12 years even if you never sell.

The pattern: exit taxes bite holdings that got big while you sat there. So sequence your moves: incorporate after you land in the low-tax country, not before you leave the high-tax one; and if a big equity stake or portfolio is coming (an exit, an IPO, two decades of ETFs), understand your country’s exit rules years ahead. A wealth-tax radar completes the picture: Spain, Norway, and Switzerland still levy net wealth taxes; the Netherlands taxes a deemed return on assets.

The covered-call and vested-RSU mechanics from Part 1 and Part 2 work from any European brokerage — the tax label on the premiums just changes by country.

Key takeaways — Part 8

No pan-European TFSA. ISA/PEA/ISK are national and don’t travel — use your country’s wrapper while you’re in it.

Take every euro of employer pension matching.

Exit taxes are the price of bad sequencing: Germany’s hits ≥1% company stakes and big ETF positions; France, Spain, Norway have their own.

Plan moves before holdings get big — mobility is a strategy only if the exits are clean.

Summary

Europe’s lever is the country. Canada = structure, US = state, Europe = the map — and only the immigrant gets to choose freely.

Employment is the anchor: high tax wedge (40–50%+), high floor (healthcare, pension, vacation) — and for immigrants, the job is the visa (Blue Card → PR in as little as 21 months in Germany).

RSUs vest as income plus social contributions; reliefs are narrow and local — check, don’t assume.

Inbound regimes are the immigrant superpower: Spain 24% flat, Portugal 20% flat, Italy 50% off, NL 30% ruling, Cyprus 0% dividends — all newcomer-only, all time-boxed. Germany has none.

Digital nomad visas exist across the south (€2,100–4,500/mo thresholds); Germany and Austria have none — and a visa is not a tax address (183 days decides).

Portugal’s citizenship path is now 10 years, not 5 — plan accordingly.

Simplified contractor regimes are hidden gems: Poland’s 12% B2B ryczałt, Portugal’s 75% rule, Czech flat tax, Bulgaria ~7.5% effective.

You cannot live in Berlin with an Estonian company — place of effective management taxes the company where you run it; e-Residency itself says so.

Misclassification is policed hard (Scheinselbständigkeit, DBA, falso autónomo) — stay genuinely independent.

The EU makes multi-country income easy: one social security (A1), reverse-charge VAT, and US contracts at ~0% withholding — US rates × European costs × a newcomer regime is the arbitrage.

Three ideal setups: the Anchor (DE/NL job + side B2B → fast PR), the Regime Surfer (ES/PT/IT flat-tax decade), the Full Independent (Cyprus non-dom) — pick by goal, check permit rules before moonlighting.

Investing is national (ISA/PEA/ISK don’t travel) and exit taxes punish bad sequencing — move before the holdings get big.

One line to remember: in North America, you optimize the structure; in Europe you optimize the map — pick the country and the regime before you pick anything else, and build the second income before you need it.

⬅️ This series: Canada Wealth Paths for Data Professionals (Part 1) · USA Wealth Paths for Data Professionals (Part 2)

General information for the 2025–2026 tax years, not tax, legal, or immigration advice. European rules change fast — several figures in this post changed while it was being researched. Confirm anything load-bearing — especially regime eligibility, permit conditions for side work, and exit-tax exposure — with qualified local professionals.

Nice overview, thanks!

I would add that it’s also important to consider your personal situation with finances and properties. For instance, a real estate you own in your home country might be taxed in your new country of residence. Italy taxes it annually with property tax (and it’s heavy, around 1% of real estate value), countries with exit tax (Canada, Australia, some European countries) tax unrealized value gain from this property if you decide to leave them after several years of residence and it could be a lot and totally uncontrollable, since real estate costs a lot, its prices fluctuate a lot, together with currency exchange rates.