USA Wealth Paths for Data Professionals

Employee, contractor, corporation, or cross-border — how your income structure changes what you keep as a data analyst, engineer, or analytics engineer.

The same job pays out very differently depending on how you are hired and which state you live in. This is Part 2 of a two-part series and a plain map of the US options — W-2 employment, stock that vests, 1099, Corp-to-Corp, the S-corp tax trick, opening a US company from Canada, why the same job pays about 2× south of the border, and where to invest what you keep. Part 1 covers Canada.

A note on roles. For simplicity I use the role of data engineer throughout. But it doesn’t matter — the same map applies to data analysts, analytics engineers, BI developers, software engineers, product managers, and more. What changes your take-home is the structure of your income, not your job title.

In Part 1 we mapped how you get paid in Canada — T4 employment, stock comp, sole proprietor, corporation, and cross-border work. The US works on the same idea (employee or contractor) but with different names, more company choices, and one famous tax trick. It also adds a twist Canada does not have: where you live changes your tax a lot.

We start with the simple default and add one layer at a time, ending on a US version of the “best of both worlds” setup.

Not tax advice. This post is general information for learning. All numbers are for the 2025–2026 tax years and change often. Rules differ by state and personal situation. Before you act, talk to a CPA (Certified Public Accountant) or tax attorney. A good accountant costs less than one mistake.

The default: W-2 employment

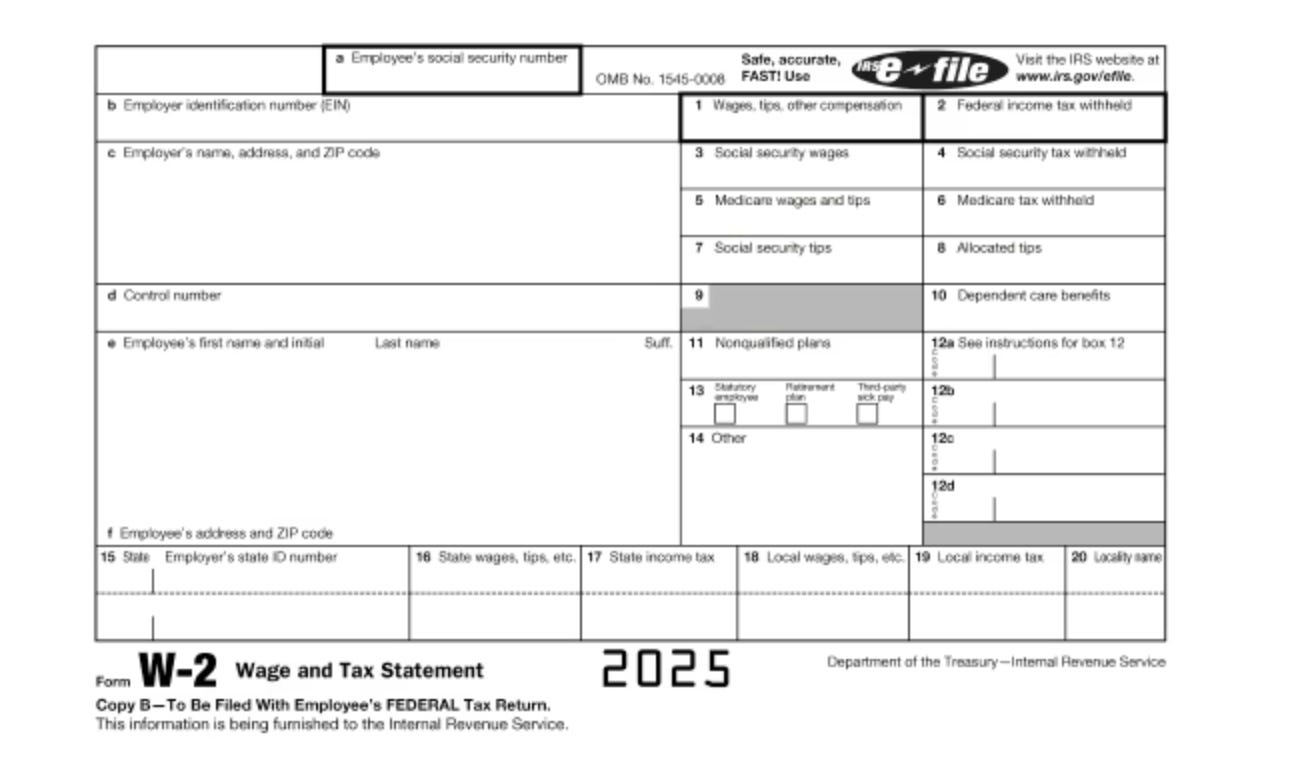

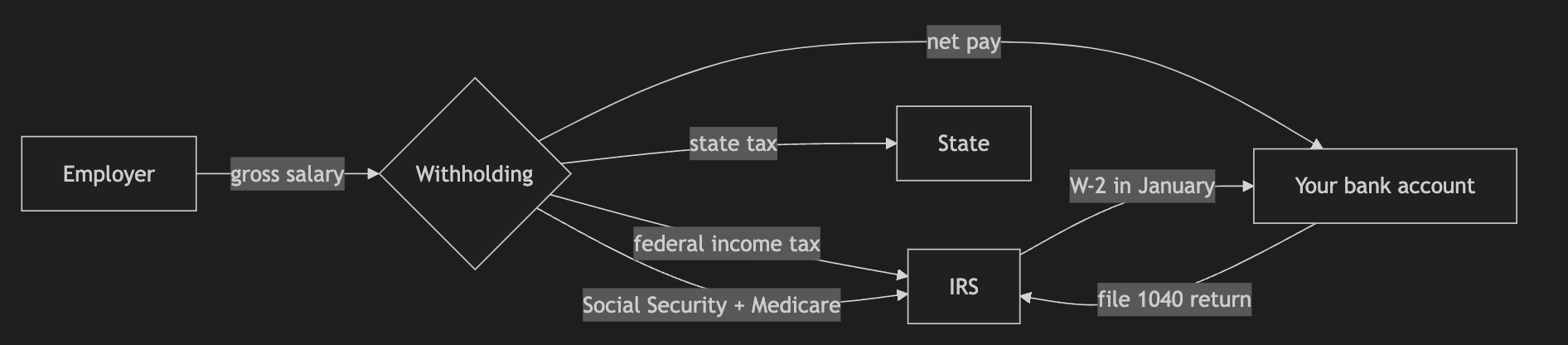

In the US, most people work as an employee of one company. The company pays you a salary and does the tax work for you. The US version of Canada’s T4 is the W-2 (the Wage and Tax Statement). A US employer issues it each January. Like the T4, it reports your wages and the tax they withheld.

The employer withholds:

Federal income tax — based on the W-4 form you fill out (the cousin of Canada’s TD1).

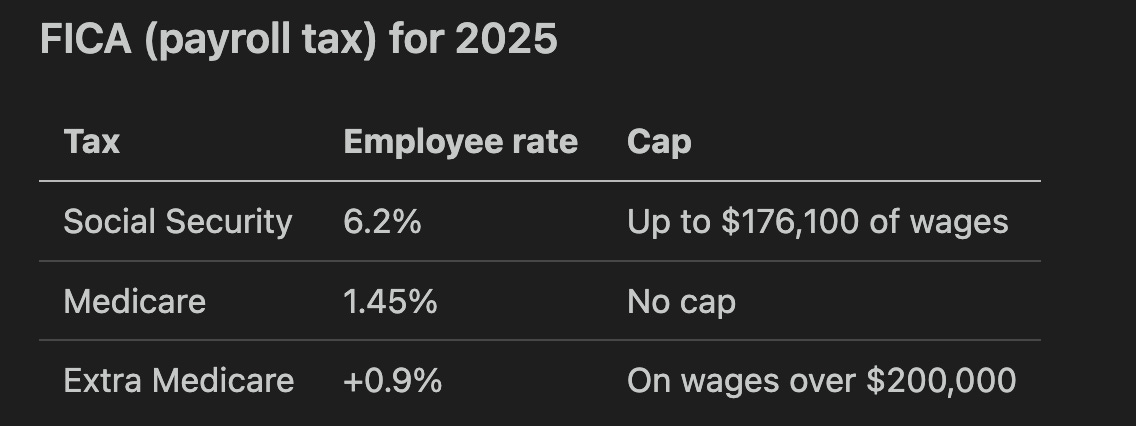

FICA — Social Security (6.2%) and Medicare (1.45%). The employer matches both.

State income tax — where the state has one.

The benefits of a W-2 job are the same as a salaried job anywhere: health insurance, a 401(k) retirement plan with a match, paid time off, and stability. You trade a higher rate (a contractor charges more) for safety and zero admin.

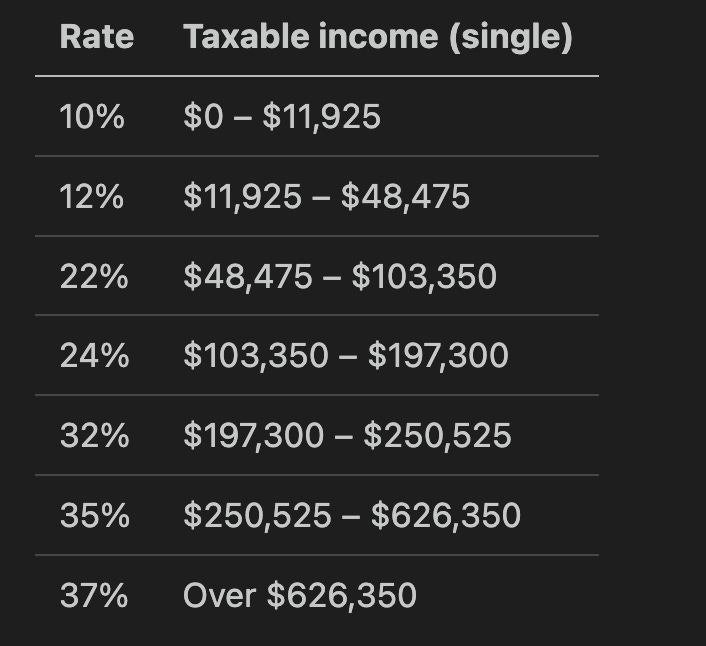

2025 federal brackets (single filer)

The US uses the same marginal idea as Canada: income is sliced into brackets, and each slice is taxed at its own rate. Only the dollars inside a higher bracket are taxed more — moving up a bracket never lowers your take-home.

The standard deduction for a single filer in 2025 is $15,750 — income below that is not taxed.

The big US difference: states

This is where the US splits from Canada. State tax varies enormously.

Nine states have no income tax at all, including Texas, Florida, and Washington.

California tops out at 13.3% on very high income. New York and New Jersey are also high.

A data engineer earning the same salary keeps much more in Austin or Seattle than in San Francisco. There is no Canadian equivalent — every Canadian province charges income tax.

The employer matches the 6.2% and 1.45%. Remember that match — when you contract, you may have to pay both halves yourself.

Tax calculators are worth using

You do not need to do this math by hand. Plug your salary and state into one of these:

SmartAsset income tax calculator — federal + state + FICA in one shot.

ADP paycheck calculator — per-paycheque take-home math.

IRS Tax Withholding Estimator — the official one; use it to tune your W-4.

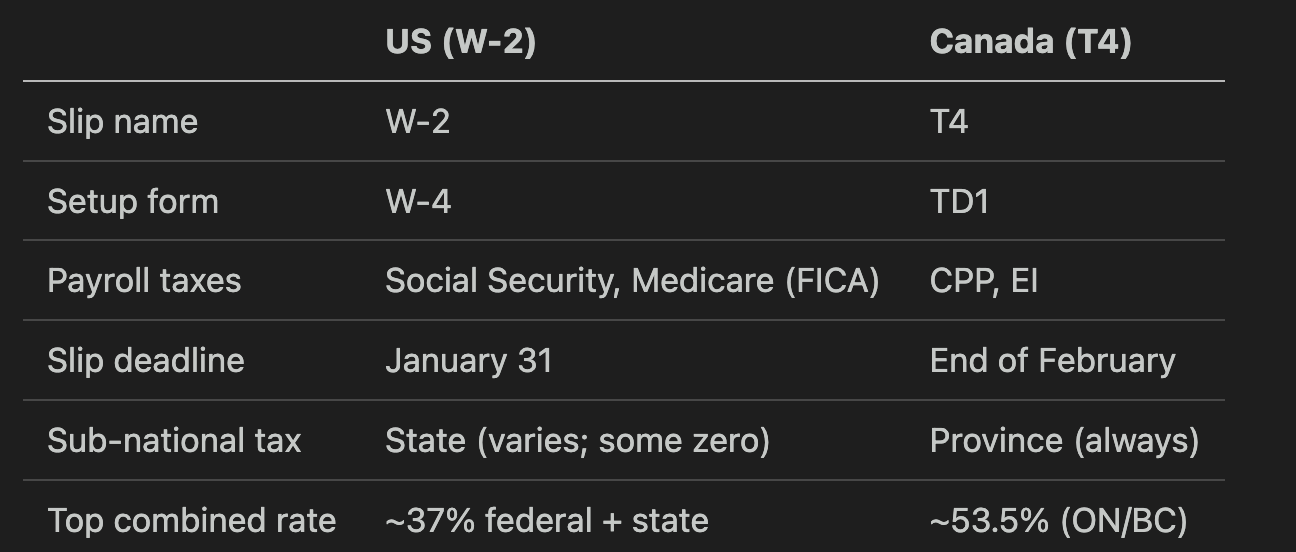

W-2 vs Canada’s T4 at a glance

W-2 vs Canada’s T4 at a glance

US (W-2)Canada (T4)Slip nameW-2T4Setup formW-4TD1Payroll taxesSocial Security, Medicare (FICA)CPP, EISlip deadlineJanuary 31End of FebruarySub-national taxState (varies; some zero)Province (always)Top combined rate~37% federal + state~53.5% (ON/BC)

Key takeaways

The W-2 is the US version of the T4. The employer withholds tax and FICA for you.

Tax is marginal, just like Canada.

State tax runs from 0% to 13.3% — where you live matters a lot.

Stock compensation: RSUs and the vesting tax

Big tech companies — Amazon, Microsoft, Google, Meta, and many others — pay a large part of the offer in stock, not just salary. For a senior data engineer, stock can be a third or even half of total pay. So you need to know how it is taxed.

The most common form is the RSU — a Restricted Stock Unit. It is a promise of company shares that you receive over time, as long as you stay.

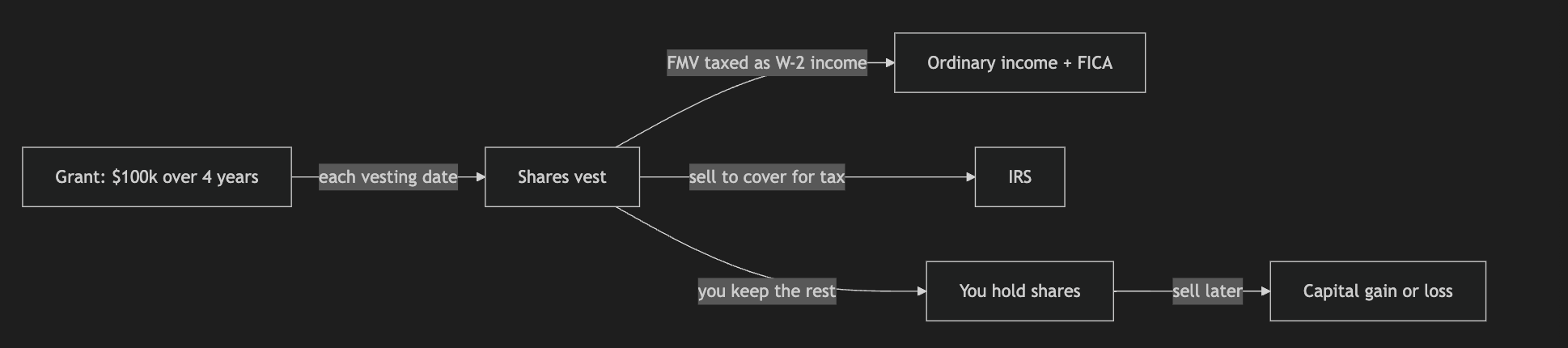

A simple example

On your hire date, the company grants you $100,000 in RSUs that vest over 4 years. “Vest” means the shares become really yours. A common schedule is 25% per year, often paid out each quarter. So roughly $25,000 of stock becomes yours each year.

The key point: on each vesting date, the value of the shares that vest is ordinary income. It is added to your W-2 wages and taxed at your normal rate, plus FICA and state tax. To pay it, the employer usually does a “sell to cover” — it sells some of the vesting shares and sends the tax to the IRS, leaving you the rest.

The 22% trap — your year-end surprise

Here is the US-specific catch. Employers withhold federal tax on RSU income at the flat 22% supplemental rate (37% on amounts over $1 million in a year). For a data engineer in the 32% or 35% bracket, 22% is not enough.

Example: a $100,000 vest is withheld at 22% = $22,000. But your real rate is ~35% = $35,000. So you owe about $13,000 more when you file. This is the classic RSU surprise. Set the gap aside, or ask payroll to withhold extra.

When you sell later

After vesting, the shares are yours. Your cost basis is the share price on the vesting date — the amount already taxed as income. When you sell:

Held more than one year after vesting → long-term capital gains (lower rates: 0%, 15%, or 20%).

Held one year or less → short-term, taxed as ordinary income.

A capital loss (selling below the vesting price) can offset other gains.

Common mistake: people forget the vesting value was already taxed and pay tax twice. You only owe capital gains on the growth after vesting.

Key takeaways

RSUs are taxed as ordinary W-2 income at vesting, plus FICA.

Default withholding is a flat 22% — too low for high earners, so expect a balance owing.

Sell after one year for the lower long-term capital gains rate.

The multiple-job tax trap (and a hidden upside)

Holding two W-2 jobs at once has the same trap as two T4s in Canada. Each job withholds as if it is your only income, so the total is under-withheld and you owe a balance in April.

There are two reasons. First, each job’s payroll applies the standard deduction, so the tax-free amount gets counted twice. Second, each job withholds at the lower brackets that fit its salary alone, but the IRS stacks both salaries and taxes the top slice at a higher rate. Neither employer can see the other.

The fix is the same idea as Canada: adjust the W-4 on your second job (there is a multiple-jobs worksheet and a checkbox for exactly this), or send the IRS quarterly estimated payments. If you underpay by enough, the IRS adds an underpayment penalty, so do not just wait until April. (Part 1 explains this trap in more detail for the Canadian case — the mechanics are the same.)

The hidden upside: two benefit plans

Two jobs are not all bad. Two employers usually mean two health plans. Through coordination of benefits, one plan pays first (primary) and the other covers much of what is left (secondary). Together they can cut your out-of-pocket costs to almost nothing — even if both employers use the same insurer.

Key takeaways

Two W-2 jobs under-withhold. Fix it on the second job’s W-4 or pay estimated tax.

Upside: two health plans that coordinate (primary + secondary).

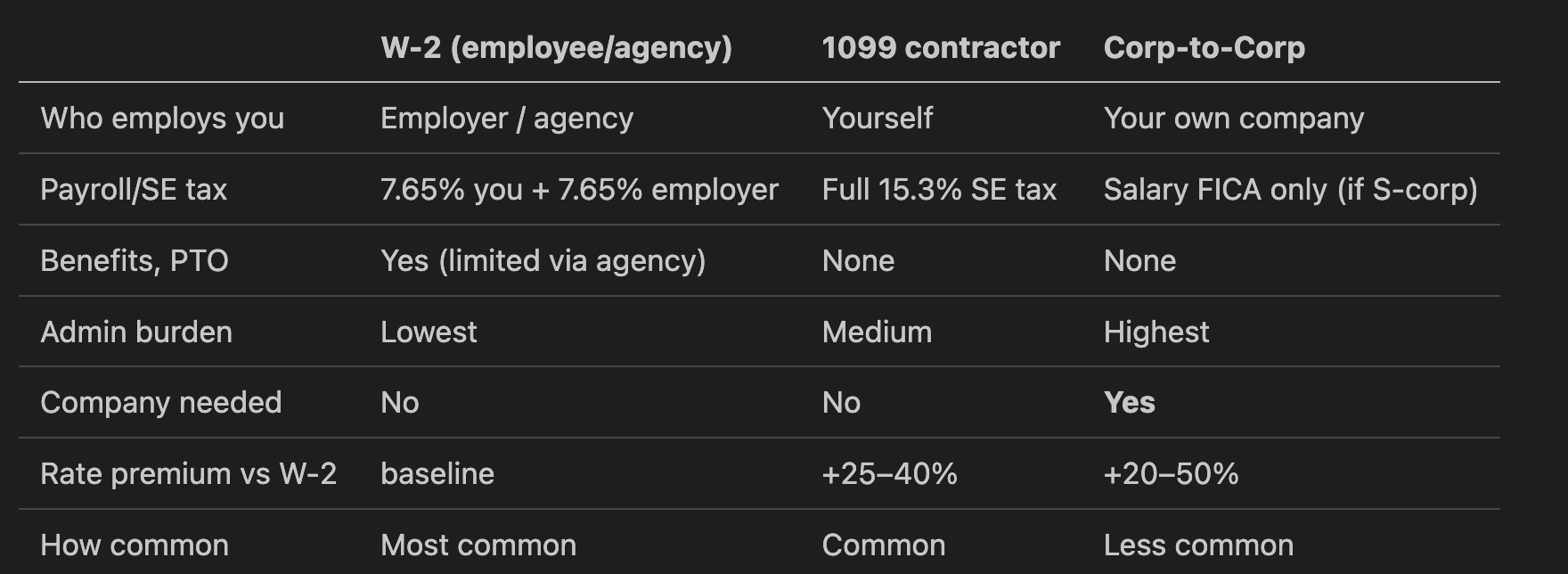

Going independent: 1099, W-2 contract, Corp-to-Corp

Now we leave employment. As a contractor in the US there are three ways to get paid.

1099 independent contractor. You work under your own name, no company. The client pays you gross and issues a 1099 form. You handle all your own tax, including self-employment (SE) tax of 15.3% — that is both halves of Social Security and Medicare, which an employer would normally split with you. You can deduct half of it, and often 20% of your business income through the QBI deduction (see Part 5). No benefits, no paid time off.

W-2 contract (through an agency). A staffing agency employs you on a W-2 and places you at a client. The agency withholds your taxes and pays the employer’s share of FICA. You get W-2 simplicity while doing contract work. This is the most common and lowest-friction contract path.

Corp-to-Corp (C2C). You own a company (an LLC or corporation) and your company contracts with the client, business to business. Highest take-home, full tax flexibility, but you carry all the admin.

Why C2C is harder to find. You must already own a company and usually carry insurance before you can sign. That filters out casual contractors. Some companies prefer C2C because it removes any “is this really our employee?” risk. Others avoid it because of vendor paperwork, and many large firms route all contractors through approved staffing agencies on W-2 instead.

Nobody withholds for you: quarterly estimated taxes

The biggest mental shift when you leave W-2: no one takes tax off the top anymore. The client pays you gross. You must send the IRS (and your state) quarterly estimated payments — four deadlines a year: April 15, June 15, September 15, and January 15. Miss them or underpay, and the IRS adds an underpayment penalty on top of the tax — even if you pay everything in April.

The working rule of thumb: set aside 25–35% of every invoice in a separate account and never touch it. The safe-harbor rule protects you: pay at least 100% of last year’s tax (110% if you earned over $150k) through the year and you avoid penalties no matter what you end up owing.

The misclassification line — the US cousin of Canada’s PSB

The US has worker misclassification, and it cuts the other way. In Canada, the risk lands on you (your corporation loses its tax advantages). In the US, the risk lands mostly on the client — if the IRS or a state decides their “1099 contractor” is really an employee, the client owes back payroll taxes and penalties.

The tests are similar on both sides of the border: who controls how and when the work is done, whose equipment is used, and whether you carry business risk and serve multiple clients. States can be stricter than the IRS — California’s ABC test (from the AB5 law) presumes you are an employee unless the client proves otherwise.

Why you should still care as the contractor: skittish clients route around the risk by refusing 1099/C2C entirely and forcing you through a W-2 agency at a lower effective rate. Looking genuinely independent — own entity, own tools, multiple clients, a real contract — keeps the better-paying doors open.

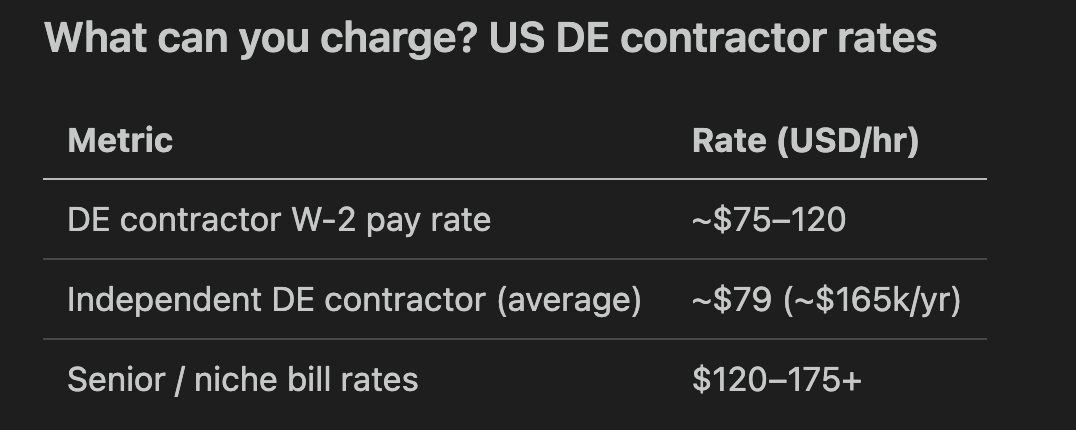

These run higher than Canadian rates, partly because US salaries are higher and the contractor self-funds benefits. A 1099 rate is usually +25–40% over the equivalent W-2 hourly; C2C is +20–50%.

Key takeaways

Three paths: 1099, W-2 contract, and Corp-to-Corp.

1099 means paying the full 15.3% self-employment tax yourself.

No one withholds for you — pay quarterly estimated taxes and set aside 25–35% of every invoice.

Misclassification is the US cousin of Canada’s PSB — stay genuinely independent to keep 1099/C2C doors open.

C2C pays the most but needs a company and insurance — and is rarer.

LLC, S-corp, C-corp, and the S-corp trick

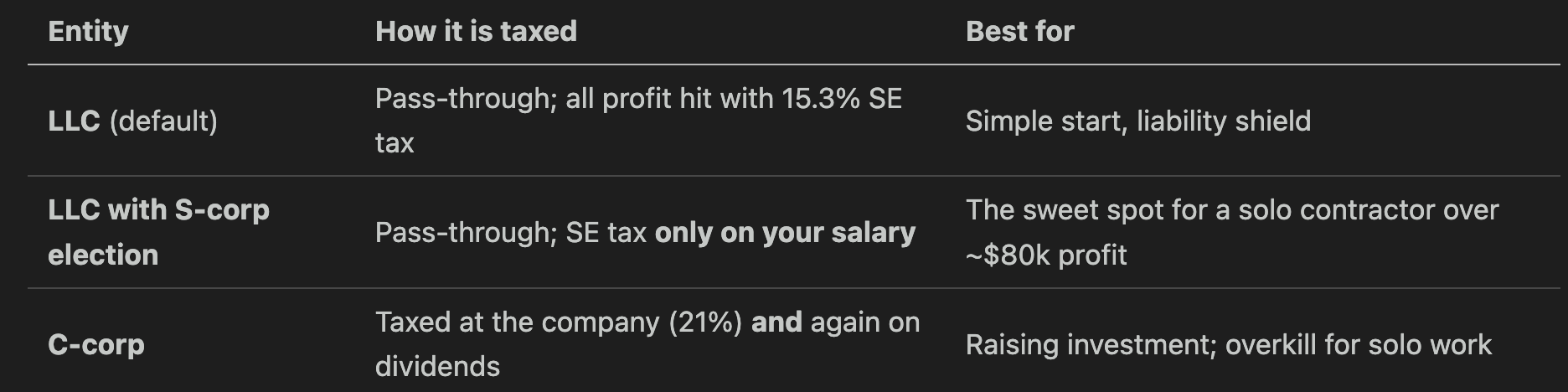

If you contract enough, you set up a company. The US has three main types.

An LLC (Limited Liability Company) is the simple default. It shields your personal assets and is easy to run. But by default all its profit is hit with the full 15.3% self-employment tax.

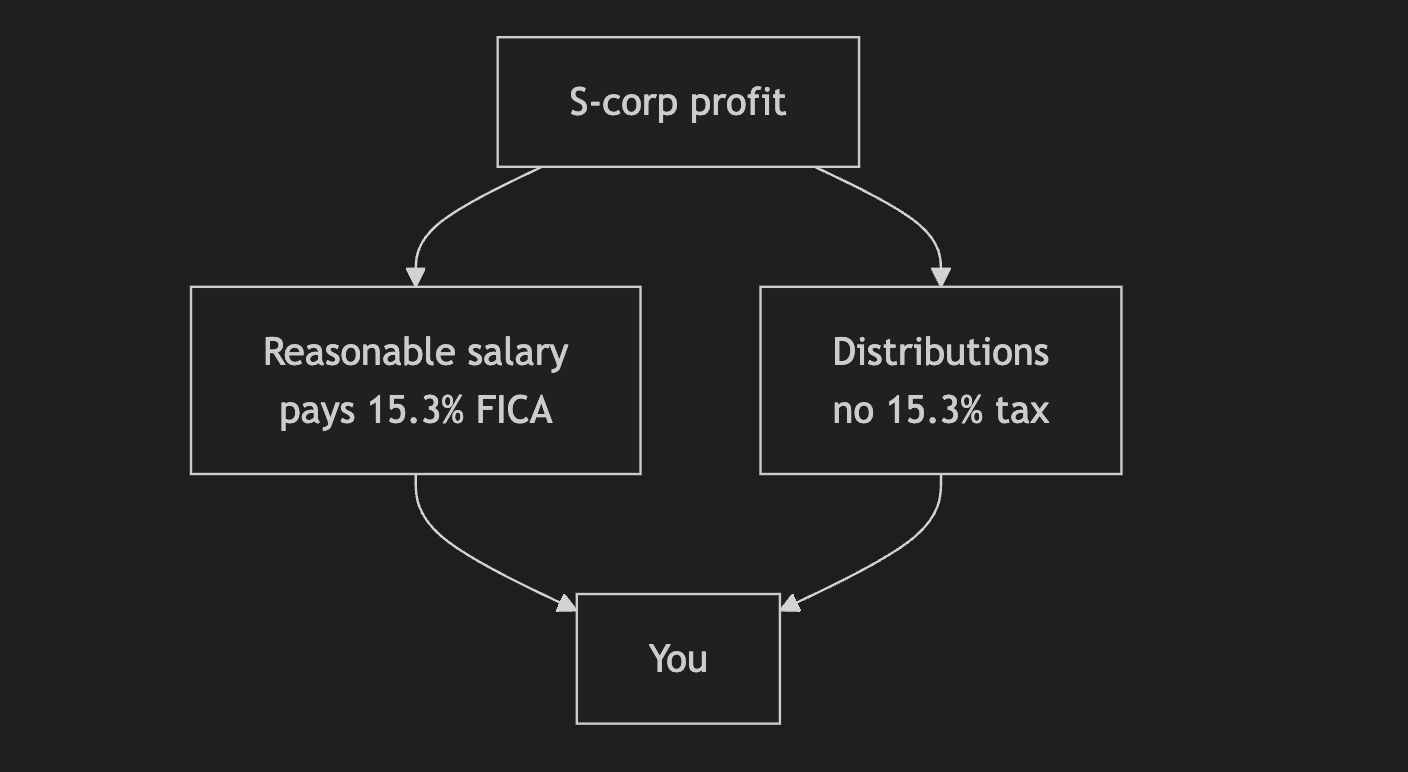

The S-corp election is the famous trick. It is the US cousin of the Canadian salary-vs-dividends choice. An S-corp lets you split your profit into two parts:

A reasonable salary — this pays the 15.3% payroll tax.

Distributions — these do not pay that 15.3% tax.

So you save ~15.3% on the distribution part. The guardrail: the salary must be reasonable — fair market value for the work you do. The IRS audits arbitrary splits. There is no safe “60/40” rule. This trick usually pays off once profit is around $80,000+, where the savings beat the extra payroll and accounting cost.

The QBI deduction (Section 199A) is another reason to contract. It lets pass-through owners deduct up to 20% of qualified business income. W-2 employees do not get it.

A C-corp is taxed at the company level (21%) and again when it pays dividends — “double taxation.” It is for businesses raising outside investment, not solo contractors.

What you can deduct

Like a Canadian corporation, a US business deducts the reasonable costs of earning its income. Common ones for a data professional:

Home office — a share of rent or mortgage interest, utilities, and internet, based on the space used (or the simplified $5/sq ft method).

Equipment — laptops and gear, often written off in full the year you buy them (Section 179 / bonus depreciation).

Software — your SaaS tools, cloud accounts, and subscriptions.

Health insurance premiums — self-employed people deduct their own premiums; W-2 folks cannot.

Half of the SE tax — the “employer half” is deductible.

Professional fees — your CPA and attorney.

Meals — generally 50% deductible.

The quiet giant: self-employed retirement accounts

This one is underrated. A W-2 employee can put $23,500 (2025) into a 401(k). A self-employed person with a Solo 401(k) contributes as both employee and employer — up to $70,000 (2025) in total, all tax-deferred. A SEP-IRA is the simpler cousin: up to 25% of compensation, same $70k ceiling, almost no paperwork.

For a contractor with strong side income, this is often worth more than the S-corp trick itself: it shelters tens of thousands per year from current tax while it compounds. (Note the interaction: Solo 401(k) employer contributions are based on your salary in an S-corp — set the salary too low and you also cap your retirement room. Another reason the split must be reasonable.)

Key takeaways

An LLC is the simple, protective default.

The S-corp salary-plus-distribution split cuts the 15.3% SE tax — once profit clears ~$80k.

The QBI deduction lets pass-through owners deduct up to 20% of business income.

Deduct home office, equipment, software, your health insurance, and half the SE tax.

A Solo 401(k) shelters up to $70k/year — often a bigger win than the S-corp trick.

Cross-border: foreign clients, and opening a US company from Canada

The US is often the client, not the home base. Many data engineers outside the US contract for US startups and get paid in US dollars through platforms like Deel, Remote.com, and Oyster. These let a company pay a worker in another country without opening a local office.

If you are in the US, you can also use these platforms to contract for companies abroad. The rule that matters: you owe income tax where you live and work, not where the client sits. A US resident pays US tax on that income, whatever country the client is in.

If you are outside the US invoicing a US company, the foreign worker files a W-8 form so the US payer does not withhold US tax, and the income is taxed in the worker’s home country under a tax treaty. Part 1 walks through this in detail for a Canadian corporation earning US dollars — the same logic works from almost anywhere.

Opening a US company from Canada

A common question from Canadian data professionals: should I open a company in the US? Here is how it actually works.

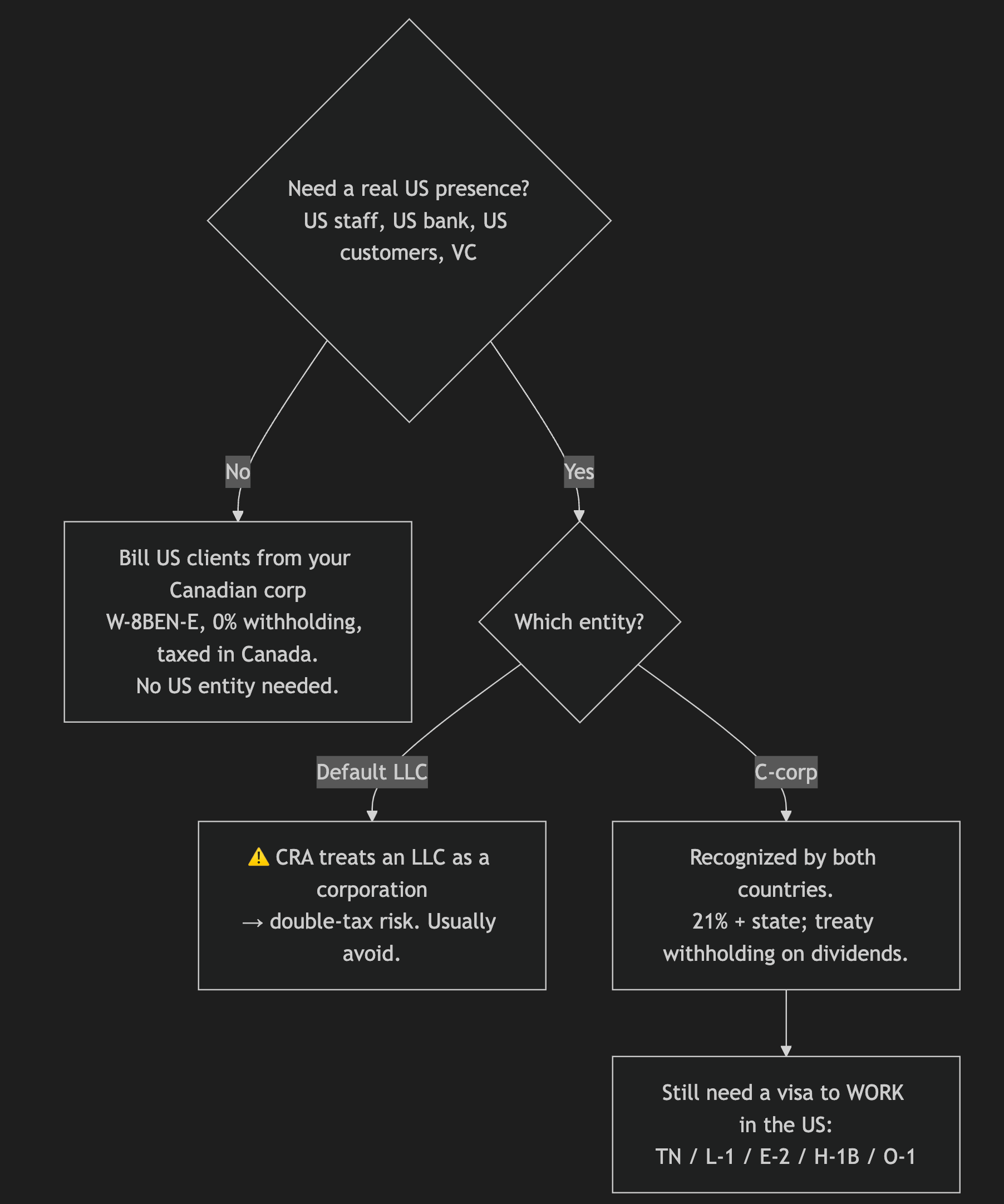

First — do you even need one? Usually not. Under the Canada–US tax treaty (Article VII), if your Canadian corporation has no permanent establishment in the US — no office, no US-based staff, no agent closing deals for you — your business profits are taxable only in Canada. So a Canadian consultant billing US clients from a laptop in Toronto generally needs no US entity at all. You file a W-8BEN-E, the US payer withholds 0%, and you are taxed at home at the ~12% small-business rate.

You open a US company only when you want a real US presence: hiring US employees, a US business bank account and address, selling to US customers or governments that require a US vendor, raising US venture capital (a Delaware C-corp is the standard investors expect), or preparing to relocate.

The good news: you do not have to be a US citizen or resident to own a US company. A Canadian can form one — usually in Delaware or Wyoming — entirely from Canada, online, in a day.

The trap: don’t default to an LLC. An LLC is the obvious pick for an American, but it is often the wrong one for a Canadian. The IRS treats a single-member LLC as a pass-through (”disregarded entity”), while the CRA treats a US LLC as a corporation. The two views don’t line up, the foreign-tax-credit machinery breaks, and you can end up taxed twice on the same income. Cross-border accountants routinely steer Canadians away from US LLCs for exactly this reason.

Cleaner options for a Canadian:

A US C-corp — both countries agree it is a corporation, so treaty treatment is clean. It pays 21% federal corporate tax plus state, and dividends back to you face treaty withholding (5% if your corp owns ≥10% of it, otherwise 15%). This is the standard when you are raising US investment.

Keep your Canadian corporation and operate cross-border under the treaty — simplest when you are just providing services.

A purpose-built cross-border structure (for example a Canadian ULC, or a US LP) designed with an accountant.

The rule: talk to a cross-border CPA before you form anything. The wrong entity is expensive to unwind.

Compliance you can’t skip. A foreign-owned US entity needs an EIN (Employer Identification Number, via Form SS-4), files US returns each year (a foreign-owned single-member LLC must file Form 5472 + a pro-forma 1120 — missing it is a $25,000 penalty), and pays state fees (Delaware franchise tax, California’s $800 annual minimum, annual reports).

⚠️ A company is not a work permit. This is the part people get wrong. Owning a US company gives you no right to live or work in the US. That takes a visa. For Canadians the common routes are TN under CUSMA/USMCA (profession-based and employer-sponsored — “data engineer” is not a named category, so it is filed under an eligible one like Computer Systems Analyst or Engineer), L-1 (transfer from your Canadian company to a US affiliate), E-2 (treaty investor who puts real capital into a US business), H-1B (the lottery), O-1 (extraordinary ability), or a green card. This is where a cross-border immigration lawyer earns their fee.

Key takeaways

Platforms like Deel let you contract across borders in either direction; you pay income tax where you live and work.

A Canadian usually needs no US entity to bill US clients — the treaty taxes the profit in Canada.

If you do open one, avoid the LLC (the CRA treats it as a corporation → double-tax risk); a C-corp or your Canadian corp is cleaner. Ask a cross-border CPA.

A US company is not a work permit — living and working there still needs a visa.

The US pay premium: the same job for about 2×

There is a reason so many Canadian data professionals look south. For the same role and seniority, US total pay is often 1.5–2× the Canadian figure — and it is paid in US dollars.

Two multipliers stack:

Bigger numbers. US base salaries for data engineers run well above Canadian ones, and big-tech stock grants are larger.

A stronger currency. In 2025–2026 one US dollar was worth about 1.40 Canadian dollars. So every US figure is already ~40% bigger the moment you convert it.

Rough market ranges for 2026 — treat these as ballpark; they vary a lot by city and company:

A Canadian senior on ~$155k CAD and a US senior on ~$200k USD are doing the same work — but the American’s pay is about $280k CAD, nearly double, before a larger RSU grant widens the gap further.

Cost of living usually helps too

The higher pay is not eaten by higher prices — for most of the US, the opposite is true. Outside the expensive coastal metros, groceries, gas, cars, electronics, dining, and especially housing are cheaper than in Toronto or Vancouver, which rank among the least affordable cities in North America.

Real estate. A family home that runs $1.1–1.4M CAD in Toronto or Vancouver is often $400–600k USD in Austin, Dallas, Raleigh, or Phoenix — cheaper even after you convert the currency.

Everyday goods. Lower sales taxes and fierce retail competition make groceries, fuel, and consumer goods noticeably cheaper across most states.

No-tax states. Texas, Florida, Washington, Tennessee, and Nevada charge no state income tax. Stack a high USD salary + 0% state tax + lower housing, and take-home purchasing power can land well over double a comparable Canadian package.

Be honest about the trade-offs

It is not a free lunch:

Healthcare is not free. You rely on an employer plan with premiums, deductibles, and copays — and a gap between jobs leaves you exposed. Budget for it. In Canada, provincial coverage is the floor no matter what. But keep in mind

The expensive metros are genuinely expensive. San Francisco, New York, Seattle, and LA carry high rent and home prices that eat into the premium — though salaries there are usually high enough to still come out ahead, and remote work lets many earn a Bay-Area salary from a cheaper state.

Higher pay can mean a higher bracket — but even the top US federal rate (37%) plus a moderate state beats Ontario/BC’s ~53.5%, and a no-tax state beats it outright.

You need the right to work there. The premium only matters if you can legally take the job.

Key takeaways

Same job, roughly 1.5–2× the pay, in USD (worth ~1.40 CAD).

Most of the US is cheaper to live in than Toronto/Vancouver — housing especially.

No-tax states push real purchasing power to 2×+.

Offsets: private healthcare, pricey coastal metros, and needing a visa.

Make the money work: 401(k), Roth, HSA, 529, and covered calls

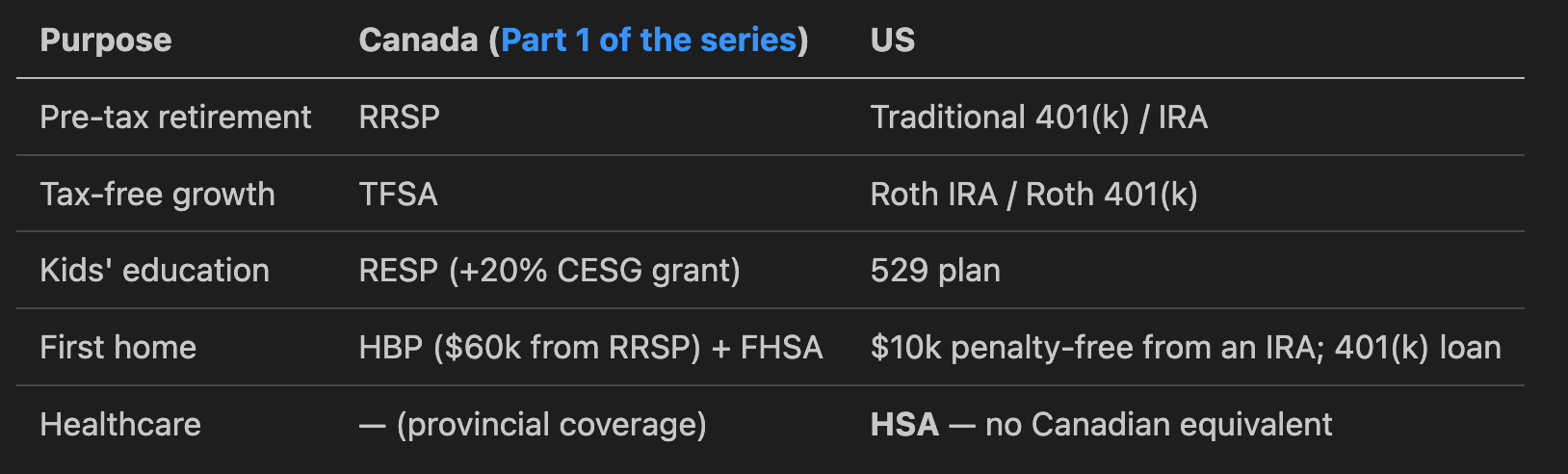

Everything so far was about how money comes in. This part is about where it goes. The US tax-advantaged account stack maps almost one-to-one onto Canada’s — here is the translation, then the plays.

401(k) — always take the match

The 401(k) is the workhorse. You defer up to $23,500 (2025) of salary pre-tax; it grows untaxed; withdrawals in retirement are taxed as income — the RRSP logic exactly. Your employer’s match is free money: contribute at least enough to capture all of it, always, before any other move.

Most plans also offer a Roth 401(k) option — pay tax now, never again. Rough rule: high earners in peak years usually prefer traditional (defer at 32–35%, withdraw cheaper later); early-career or low-income years favor Roth.

Roth IRA — the TFSA of the US (with a backdoor)

The Roth IRA is the tax-free bucket: $7,000/year (2025), no deduction going in, but zero tax forever on growth and withdrawals.

The catch a data engineer hits fast: direct contributions phase out around $150k of income (single). The workaround is famous and legal — the backdoor Roth: contribute after-tax to a traditional IRA, then convert to Roth. And big-tech plans (Amazon, Microsoft, Google, Meta all support it) offer the mega backdoor Roth: after-tax 401(k) contributions above the normal limit, converted to Roth inside the plan — pushing your total sheltered space toward the $70,000 overall cap.

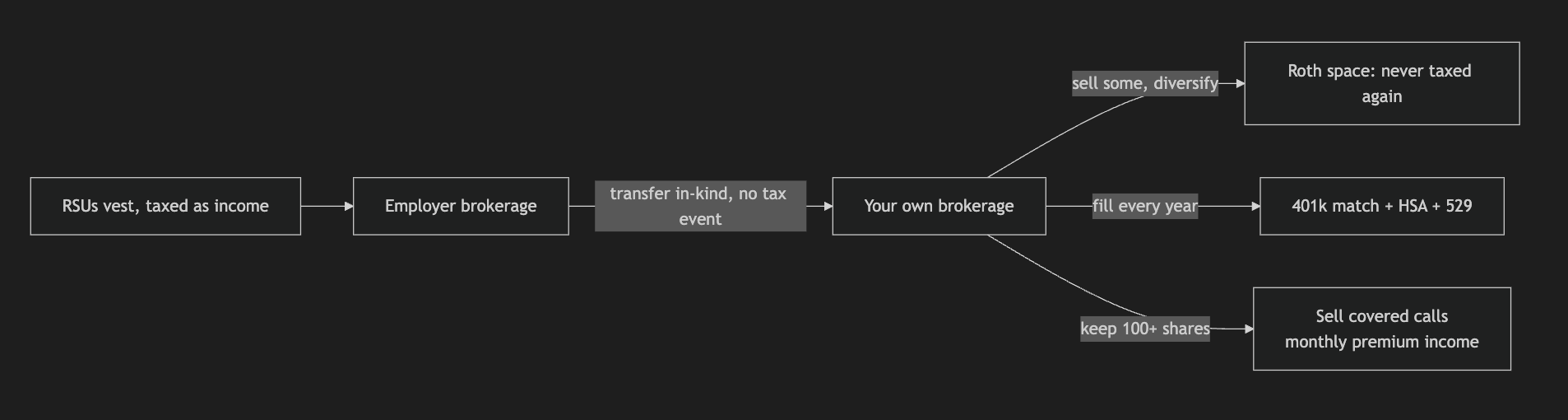

The RSU play works the same as Canada’s TFSA move: as shares vest, sell some, fill your Roth space, reinvest. The vesting tax is already sunk; everything after is growth that is never taxed again — and you cut your employer-stock concentration in the same trade.

HSA — the best tax deal in America

If your employer offers a high-deductible health plan, the HSA (Health Savings Account) is the only triple-tax-free account in the code: deductible going in, tax-free growth, tax-free out for medical costs. Limits for 2025: $4,300 individual / $8,550 family.

The power move: pay small medical bills out of pocket, invest the HSA and let it compound — after 65 it behaves like a traditional IRA for any purpose. Canada has nothing like it; if you move south, learn it.

529 — the college fund

The 529 plan is the RESP’s cousin: contributions grow tax-free and come out tax-free for education. There is no federal match like Canada’s CESG, but most states give a state-tax deduction for contributions, and the SECURE 2.0 rules added a great escape hatch: up to $35,000 of leftover 529 money can roll into the kid’s own Roth IRA — so overfunding is no longer a trap.

Covered calls — extra income from vested RSUs

Same play as Canada, same mechanics. After vesting, transfer the shares in-kind (no sale, no tax event) from the employer’s brokerage to your own. With 100+ shares, sell covered calls: collect a premium for agreeing to sell at a higher strike.

Stock stays below the strike → keep premium and shares, repeat next month.

Stock jumps above → shares are called away at the strike; you keep the premium plus the gain to the strike.

US-specific tax notes: option premiums are generally short-term gains (ordinary rates), and closing trades around your long shares can trip the wash-sale rule — keep the bookkeeping clean. Company trading windows and blackout policies apply to options on your employer’s stock too. And the honest caveat is unchanged: covered-call income is not a reason to stay concentrated in your employer — a layoff and a stock drop tend to arrive together.

The house angle

No US account matches Canada’s HBP exactly, but the pieces exist: a first-time buyer can pull $10,000 penalty-free from an IRA, and many borrow from their 401(k) (up to $50k, repaid to yourself with interest). Once you own, mortgage interest is an itemized deduction (on up to $750k of loan) — and if you work from home self-employed or through your company, the home-office share of mortgage interest, property tax, and utilities is a business expense (Form 8829), echoing the deduction list.

Key takeaways

401(k) first — never leave the match on the table; $23,500 deferral, $70k total space with mega backdoor.

Roth IRA is the US TFSA — use the backdoor above ~$150k income; sell vested RSUs into Roth space and the growth is never taxed again.

HSA is the only triple-tax-free account — invest it, don’t spend it.

529 for kids: state deductions now, tax-free for school, $35k Roth rollover if they don’t need it.

Covered calls on vested shares work here too — premiums are short-term gains; mind wash sales and blackout windows.

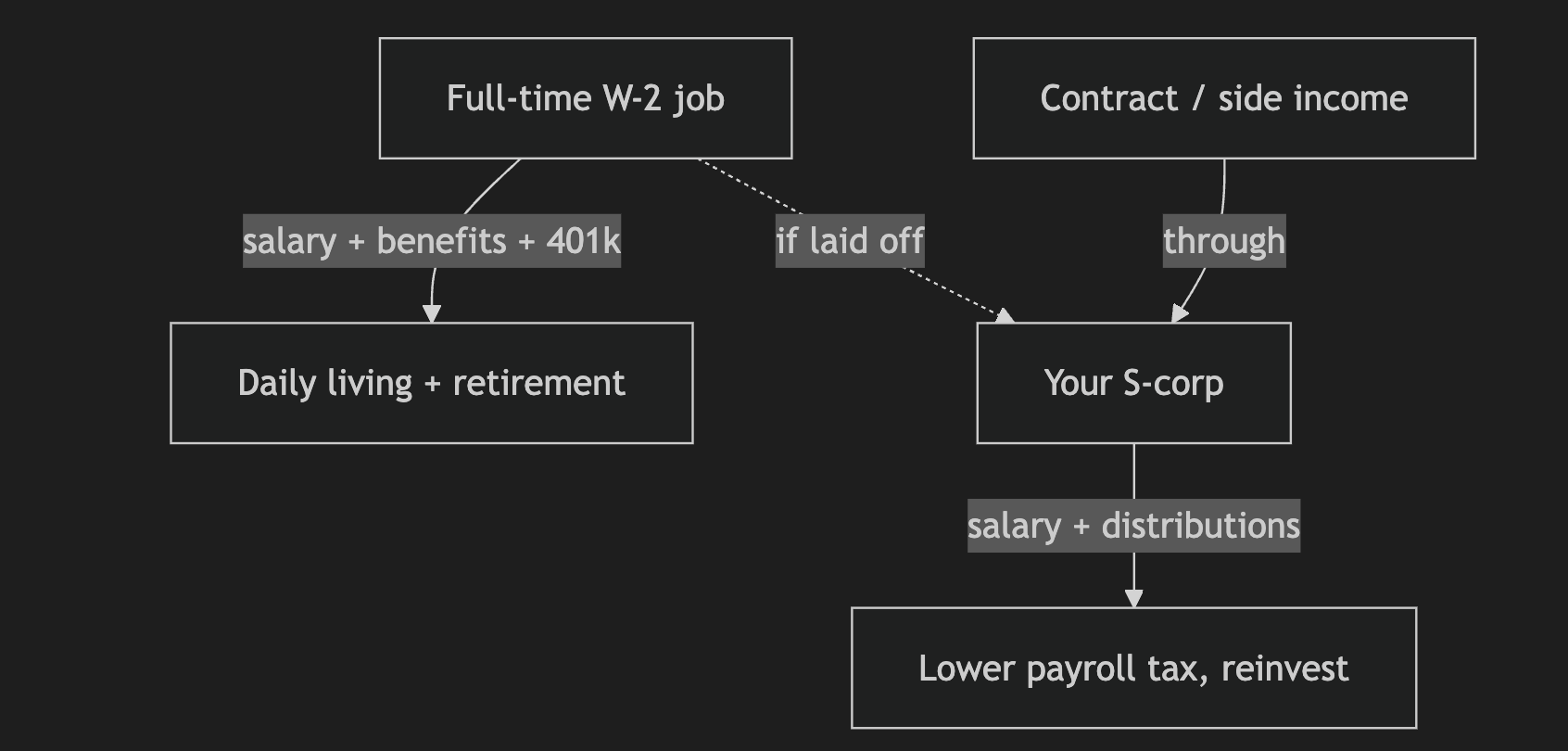

The best setup: keep the W-2, run the S-corp

Put it all together. After looking at every option, one combination is the most resilient for many data engineers.

Keep a full-time W-2 job — and run a company (S-corp) on the side.

Why: job security is a myth

Start with the honest reason. No one gives you job security. US tech layoffs proved it — big, profitable companies cut tens of thousands of well-paid engineers in a single morning, RSUs and all. Your “stable” job can end with little notice. The only real security is the kind you build yourself: a second income stream and a business that survives a layoff.

A full-time job plus a company is exactly that. Each half covers the other’s weakness:

The full-time job gives you:

A steady salary and benefits — health insurance, paid time off.

Stability — a base income while it lasts.

A 401(k) match — free retirement money.

A predictable tax situation.

The company gives you:

A place to put contract work, side projects, or any business income.

The S-corp split to cut self-employment tax on that extra income.

The QBI deduction on business profit.

A Solo 401(k) on the side income — extra retirement room on top of the day job’s 401(k) (the employee limit is shared across plans, but the employer contributions are not).

A landing pad if the job disappears — you already have an entity and clients.

You live off the job’s salary and benefits. The side income flows through your company, taxed more efficiently, and you reinvest it. If you are laid off, the company is ready to take on full-time contract work right away.

Be honest about the limits:

Reasonable salary still applies. An S-corp split has to be defensible. The IRS audits owners who pay themselves almost nothing.

It is real work. Holding a job and a real business takes time. Do not let the side business quietly become a second unpaid full-time job.

It depends on your numbers. The S-corp savings only beat the extra cost once side profit is meaningful (~$80k+). Below that, 1099 or staying W-2-only can be simpler.

Check your state. Some states tax S-corps or charge LLC fees (California’s $800 minimum, for example). Run the math for where you live.

For many mid-to-senior US data engineers, this is the sweet spot: the safety of employment, plus a tax-efficient engine — and a safety net — for everything extra you build.

Summary

W-2 employment is the simple default — the US version of the T4. The employer withholds tax and FICA.

Tax is marginal, like Canada — but state tax runs 0% to 13.3%, so location matters a lot.

RSUs are taxed as ordinary income at vesting; default withholding is a flat 22%, too low for high earners — so expect a bill. Sell after a year for long-term capital gains.

Two W-2 jobs under-withhold — fix it on the second W-4 — but they also give you two health plans that coordinate.

Contracting has three forms: 1099, W-2 contract, and Corp-to-Corp. Once you leave W-2, nobody withholds — pay quarterly estimated taxes and set aside 25–35% of every invoice.

An LLC is the simple, protective default; all its profit faces the 15.3% SE tax. Stay genuinely independent — misclassification rules (like California’s ABC test) are the US cousin of Canada’s PSB.

The S-corp trick splits profit into salary + distributions to cut that 15.3% tax — once profit clears ~$80k.

The QBI deduction (20% of business income) and a Solo 401(k) (up to $70k/year sheltered) are the self-employment perks W-2 workers never see.

Cross-border work goes both ways via Deel-type platforms; you pay tax where you live — and a Canadian usually needs no US entity to bill US clients.

Opening a US company from Canada is possible but often unnecessary; avoid the LLC trap (the CRA treats it as a corporation), a C-corp is cleaner, and a company is not a work permit.

The US pay premium is real — roughly 2× in USD, plus cheaper living and no-tax states — offset by private healthcare, pricey coastal metros, and visa hurdles.

Put the money in the right buckets: 401(k) match first, backdoor/mega-backdoor Roth for tax-free-forever growth, HSA (triple tax-free), and a 529 for the kids. Sell vested RSUs into Roth space; sell covered calls on the shares you keep.

The strongest setup for many: keep a full-time W-2 job for stability and benefits, and run an S-corp for everything extra — because job security is a myth and you build your own.

One line to remember: the job pays for your life; the company makes your extra income tax-efficient and gives you a safety net — and an hour with a good accountant pays for itself many times over.

⬅️ Start of this series: Canada Wealth Paths for Data Professionals (Part 1) — T4, RSUs, sole prop, corporations, GST/HST, and earning USD from a Canadian corp.

General information for the 2025–2026 tax years, not personal tax or legal advice. Rules change and differ by state and situation. Confirm anything load-bearing — especially S-corp reasonable-salary levels and your state's rules — with a qualified accountant.