Canada Wealth Paths for Data Professionals

Employee, contractor, corporation, or cross-border — how your income structure changes what you keep as a data analyst, engineer, or analytics engineer

You can do the same data analyst/data engineering/analytics engineer job several different ways. Each one changes how much tax you pay, how much risk you carry, and how much you keep. This post is a plain map of those options in Canada — employee, contractor, corporation, and cross-border work. In the next articles, we will cover the United States and Europe.

For simplicity, I will use the role of data engineer. But it doesn’t matter. It is applicable for product managers, software engineers, BI developers and so on.

Most data engineers learn Spark, dbt, and Snowflake. Very few learn how their pay is taxed. That is a mistake, because the structure of your income can change your take-home by tens of thousands of dollars a year.

This is Part 1 of a multi-part series. Here we map how a data engineer can work and get paid in Canada: as an employee, as a contractor, through a corporation, and even invoicing US clients in US dollars. Part 2 covers the United States. We start with the simple default and add one layer at a time, ending on a setup that combines the best parts of all of them.

Not tax advice. This post is general information for learning. All numbers are for the 2025–2026 tax years and change often. Rules differ by province and personal situation. Before you act, talk to a CPA (Chartered Professional Accountant) or tax lawyer. A good accountant costs less than one mistake.

The default: T4 employment

In Canada, most people work as an employee. You sign on with one company. They pay you a salary. This is the default, and for good reason — it is simple and safe.

When you are an employee, your employer does the tax work for you. This is called withholding at source, or “source deductions.” Every paycheque, the employer takes money off the top and sends it to the government. They withhold three things:

Income tax — federal and provincial.

CPP — the Canada Pension Plan. It pays you a pension when you retire.

EI — Employment Insurance. It pays you if you lose your job.

At the start of a job you fill out a TD1 form (the Personal Tax Credits Return). It tells the employer how much of your pay is tax-free, so they know how much to withhold. Remember this form — it causes a real problem later in the US article.

After year-end, by the end of February, your employer gives you a T4 slip. The official name is the Statement of Remuneration Paid. It is one page that reports, for that employer only, how much they paid you and how much tax, CPP, and EI they already took off.

You get one T4 per employer. You report all of them on your tax return (the T1). Then the Canada Revenue Agency (CRA) — the federal tax agency — checks what was withheld against what you really owe. If too much came off, you get a refund. If too little came off, you owe a balance.

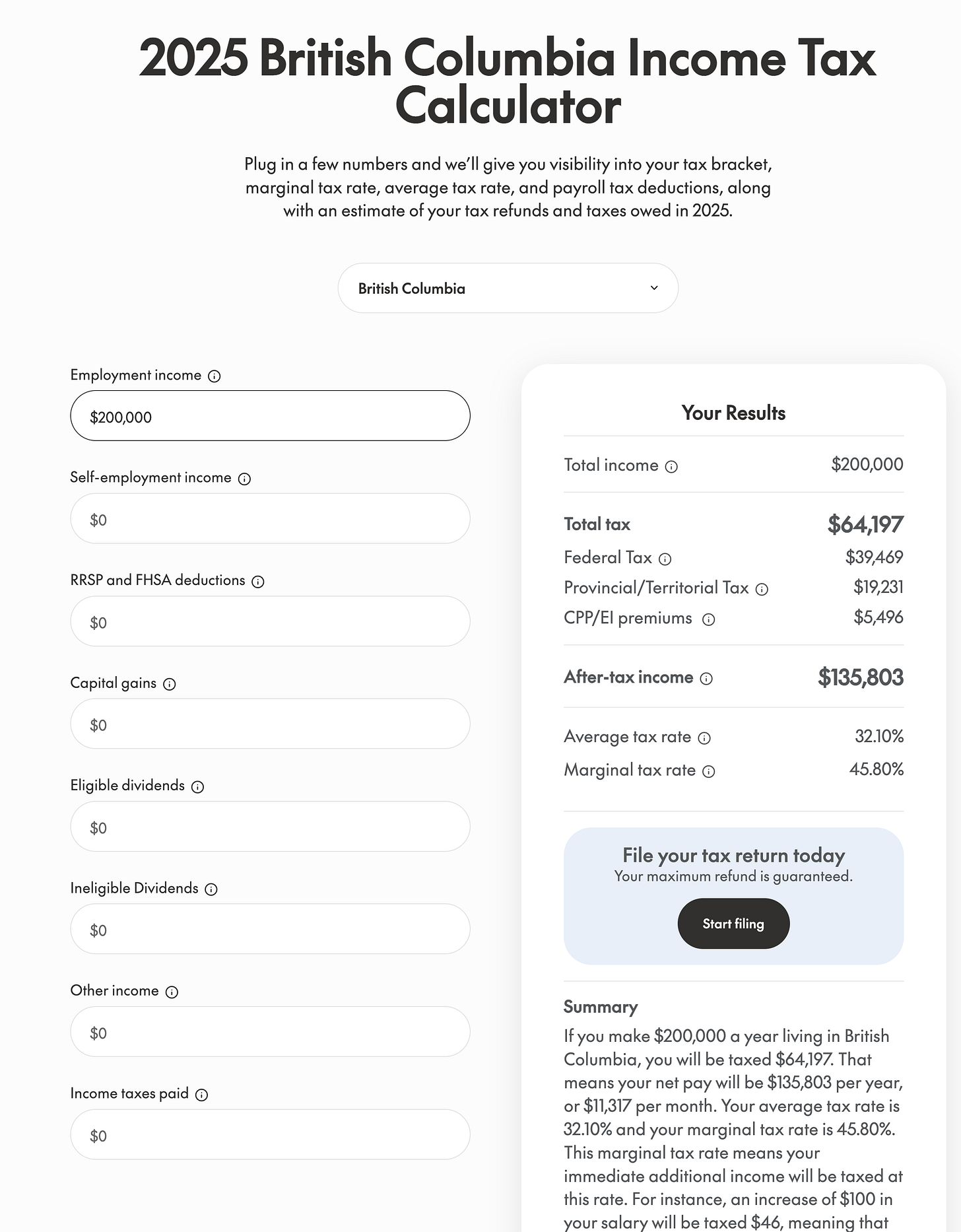

How the tax brackets work

Canada uses a progressive, marginal tax system. This is the single most misunderstood idea in personal finance, so let us be clear.

Your income is cut into slices called brackets. Each slice is taxed at its own rate. Your whole income is not taxed at one rate. The rate on your last dollar is your marginal rate. The blended rate you actually pay across all your income is your effective rate, and it is always lower.

The key takeaway: moving into a higher bracket never lowers your take-home pay. Only the dollars inside the higher bracket get taxed more. Earning one more dollar is never a net loss.

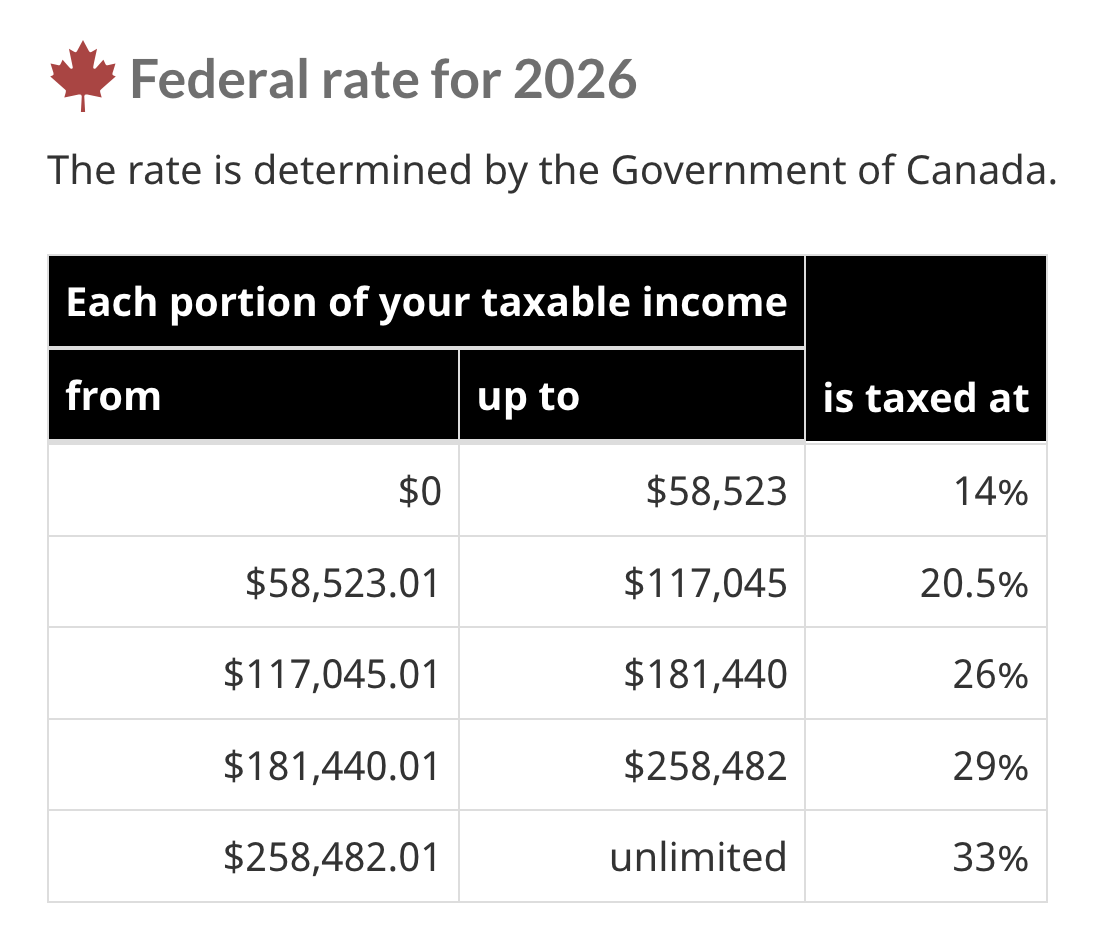

Here are the 2026 federal brackets.

The first ~$16,129 is effectively federally tax-free. This is the basic personal amount (BPA).

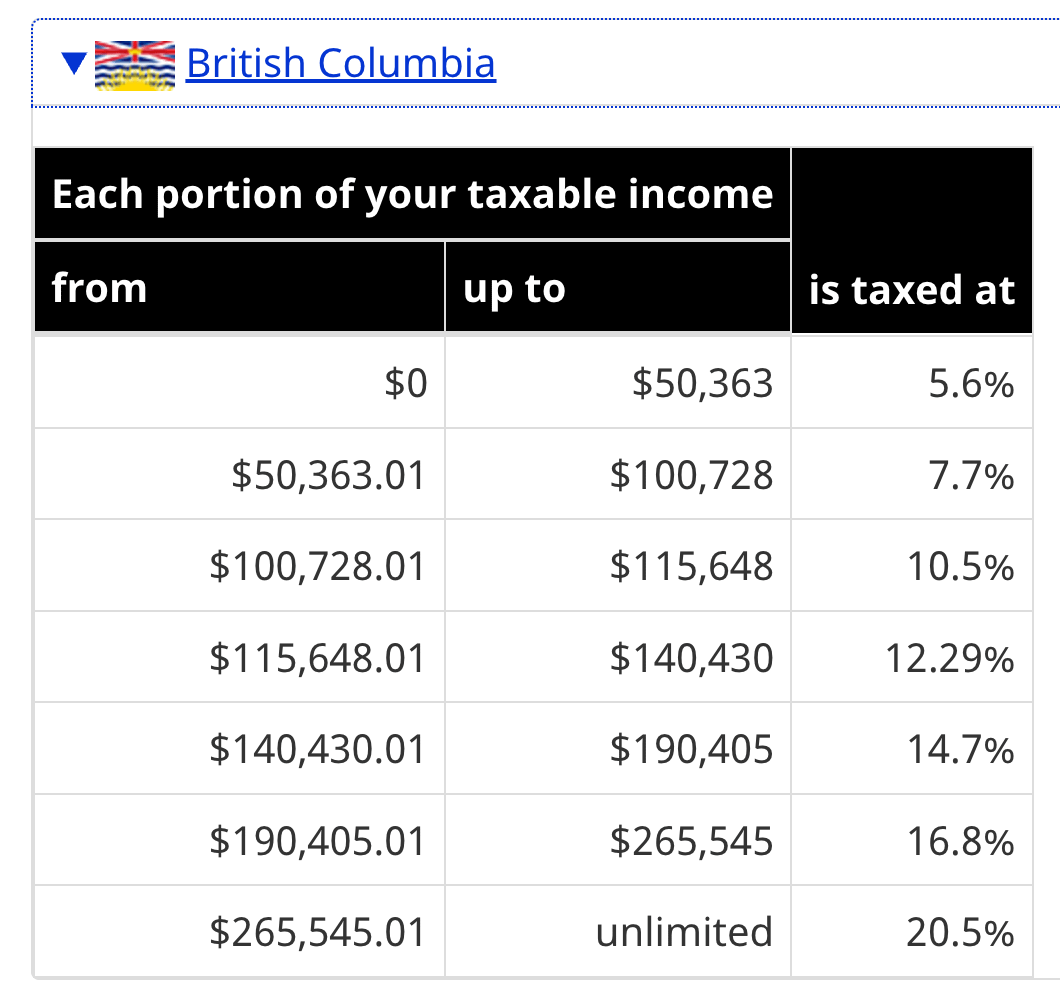

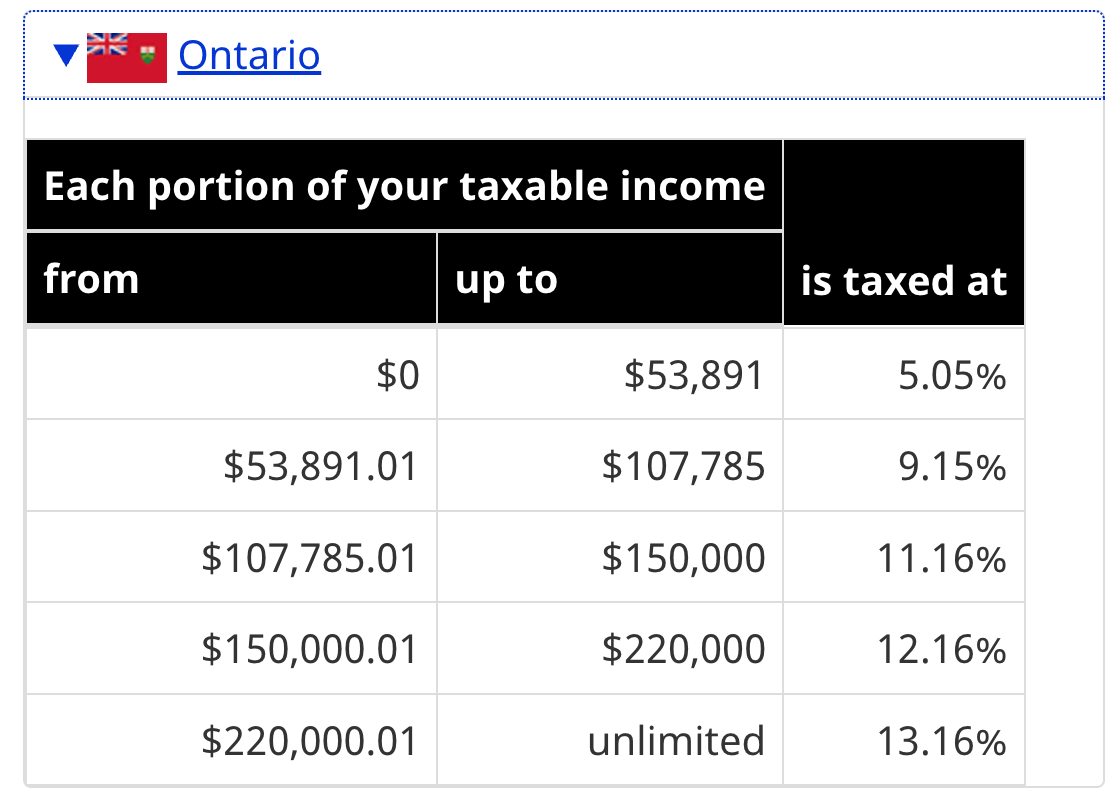

On top of federal tax, every province adds its own tax with its own brackets. Your real rate is federal plus provincial, combined. Two examples for 2026:

So a senior data engineer in Toronto or Vancouver pays about 53 cents of tax on their highest dollar. That number matters a lot when we talk about corporations later.

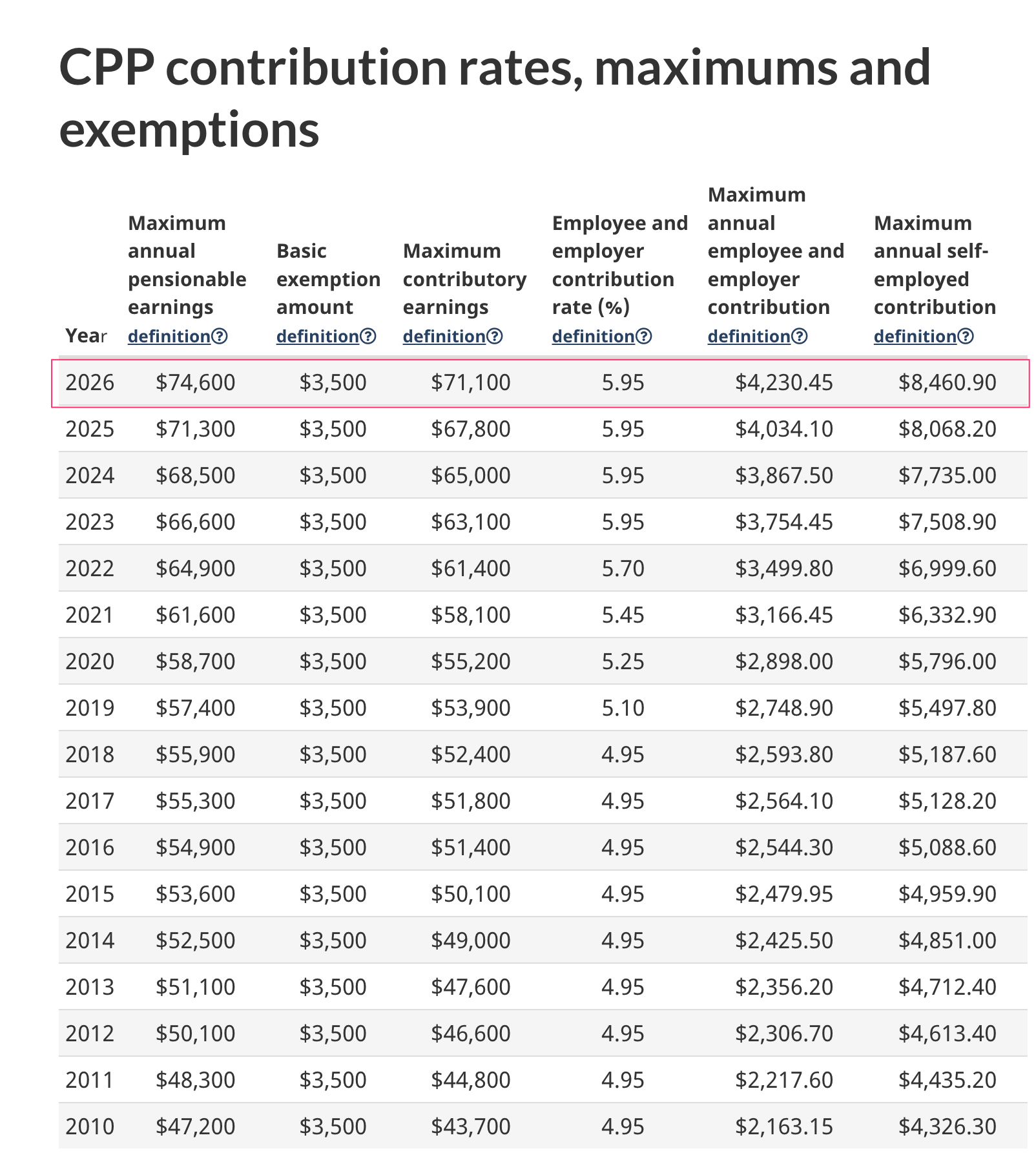

CPP and EI in 2025

These are separate from income tax. The maximums for 2026:

Your employer matches your CPP dollar-for-dollar and pays 1.4× your EI. That is part of the hidden cost of an employee that you pay yourself once you contract.

Tax calculators worth using

You do not need to do this math by hand. Plug your salary and province into one of these:

Wealthsimple income tax calculator

CRA Payroll Deductions Calculator (PDOC) — the official one, for paycheque math.

Key takeaways

As an employee you get a T4; the employer withholds tax, CPP, and EI for you.

Tax is marginal: only the dollars in a higher bracket are taxed more.

Top marginal rate in Ontario/BC is about 53.5%.

The CRA reconciles everything when you file the T1.

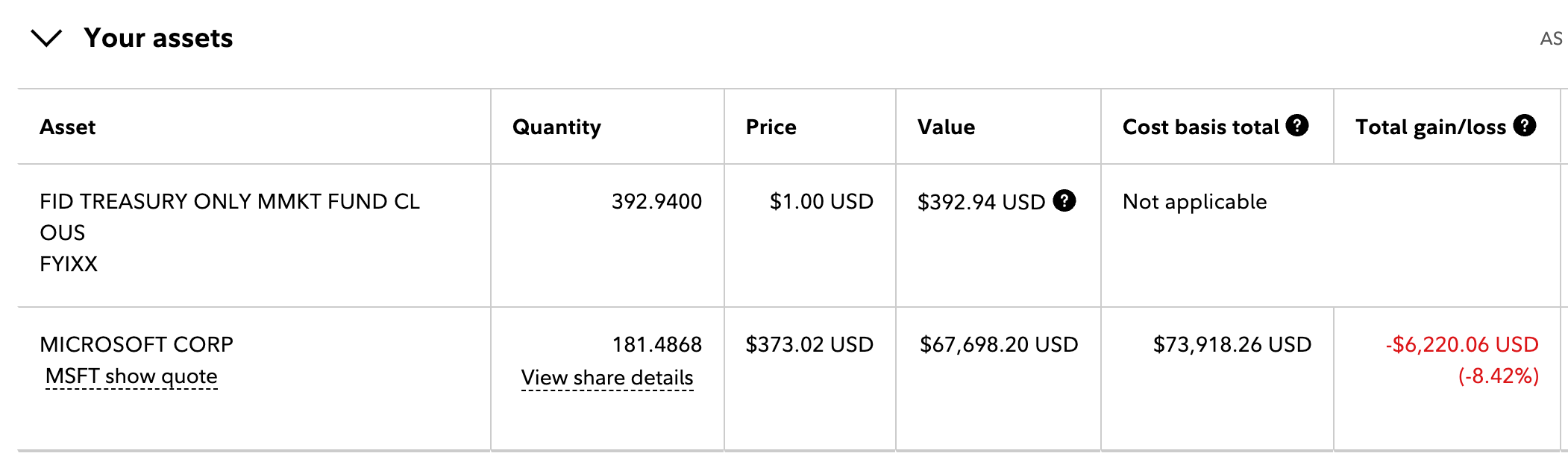

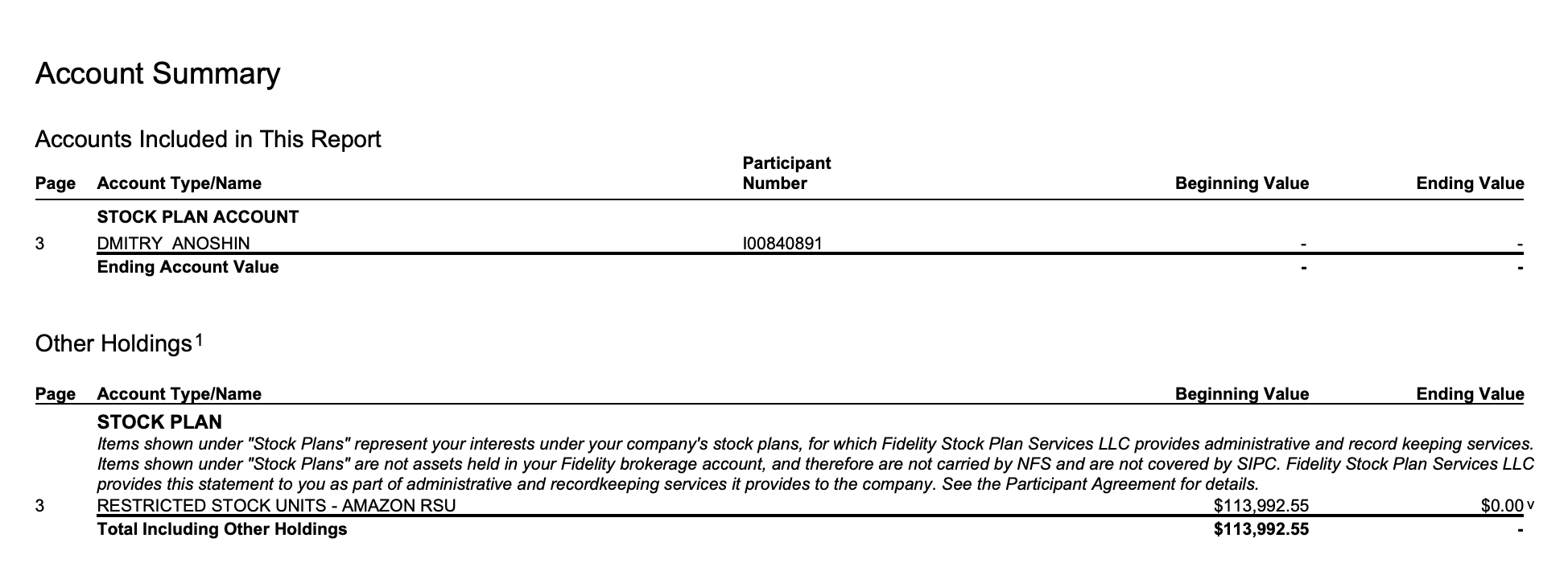

Stock compensation: RSUs and the vesting tax

Big tech companies — Amazon, Microsoft, Google, and many others — do not pay you in salary alone. A large part of the offer is stock. For a senior data engineer, stock can be a third or even half of total pay. So you need to understand how it is taxed, because the surprise is real.

The most common form is the RSU — a Restricted Stock Unit. An RSU is a promise of company shares that you receive over time, as long as you stay.

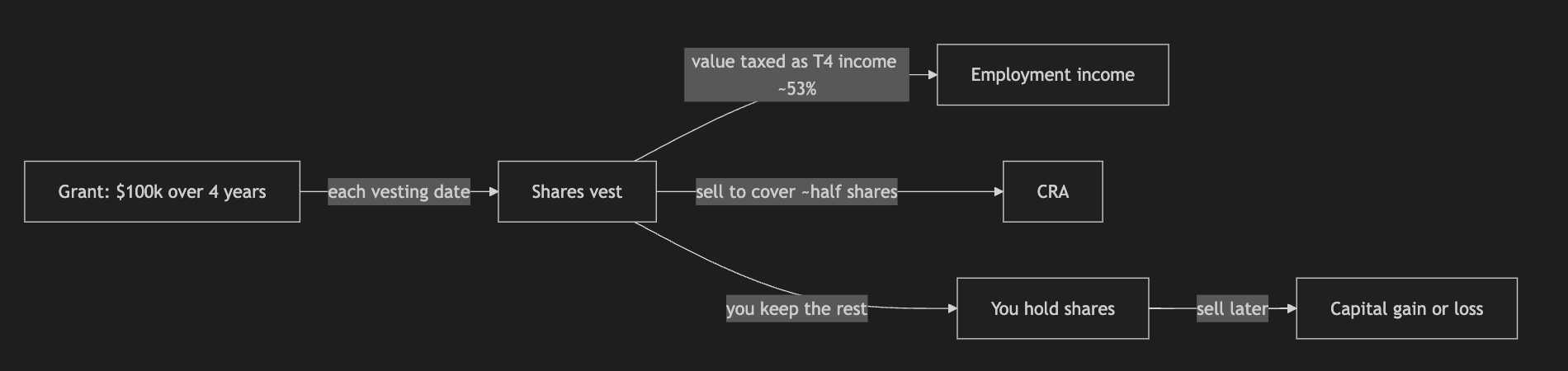

A simple example

On your hire date, the company grants you $100,000 USD in RSUs that vest over 4 years. “Vest” means the shares stop being a promise and become really yours. A common schedule is 25% per year, often paid out each quarter. So roughly $25,000 of stock becomes yours each year.

Here is the part people miss.

On each vesting date, the value of the shares that vest is treated as employment income. It is just like salary. It goes on your T4 and is taxed at your marginal rate — which for a senior data engineer is about 53%.

So the government takes its cut the moment the stock vests, not when you sell. To pay that tax, your employer usually does a “sell to cover.” It automatically sells about half of the vesting shares, sends the tax to the CRA, and leaves you the rest. That is why people say “half my stock disappears the day it vests” — that half went to tax.

Watch for the year-end surprise

The sell-to-cover withholding is not always enough. A big vest can push your income into a higher bracket, and the automatic rate the employer uses can fall short of your real ~53%. The gap shows up as a balance owing when you file — the same kind of surprise as the two-job problem.

When you sell later

After the shares vest, they are yours to keep or sell. Your cost basis (your starting value) is the share price on the vesting date — the amount already taxed as income.

When you sell:

Sell higher than the vesting price → the difference is a capital gain.

Sell lower → the difference is a capital loss, which can offset other capital gains.

In Canada, only 50% of a capital gain is taxable. This is the inclusion rate. (A proposed increase to 66.67% was cancelled in 2025, so it stays at 50%.)

Common mistake: people forget the vesting value was already taxed as income, then pay tax a second time on the whole sale amount. Keep your vesting statements. You only owe capital gains tax on the growth after vesting.

Key takeaways

RSUs are taxed as employment income at vesting, at your marginal rate (~53%).

Employers sell ~half the shares to cover the tax (”sell to cover”).

Withholding can fall short → a balance owing at tax time.

Selling later gives a capital gain or loss, taxed at the 50% inclusion rate.

The multiple-job tax trap

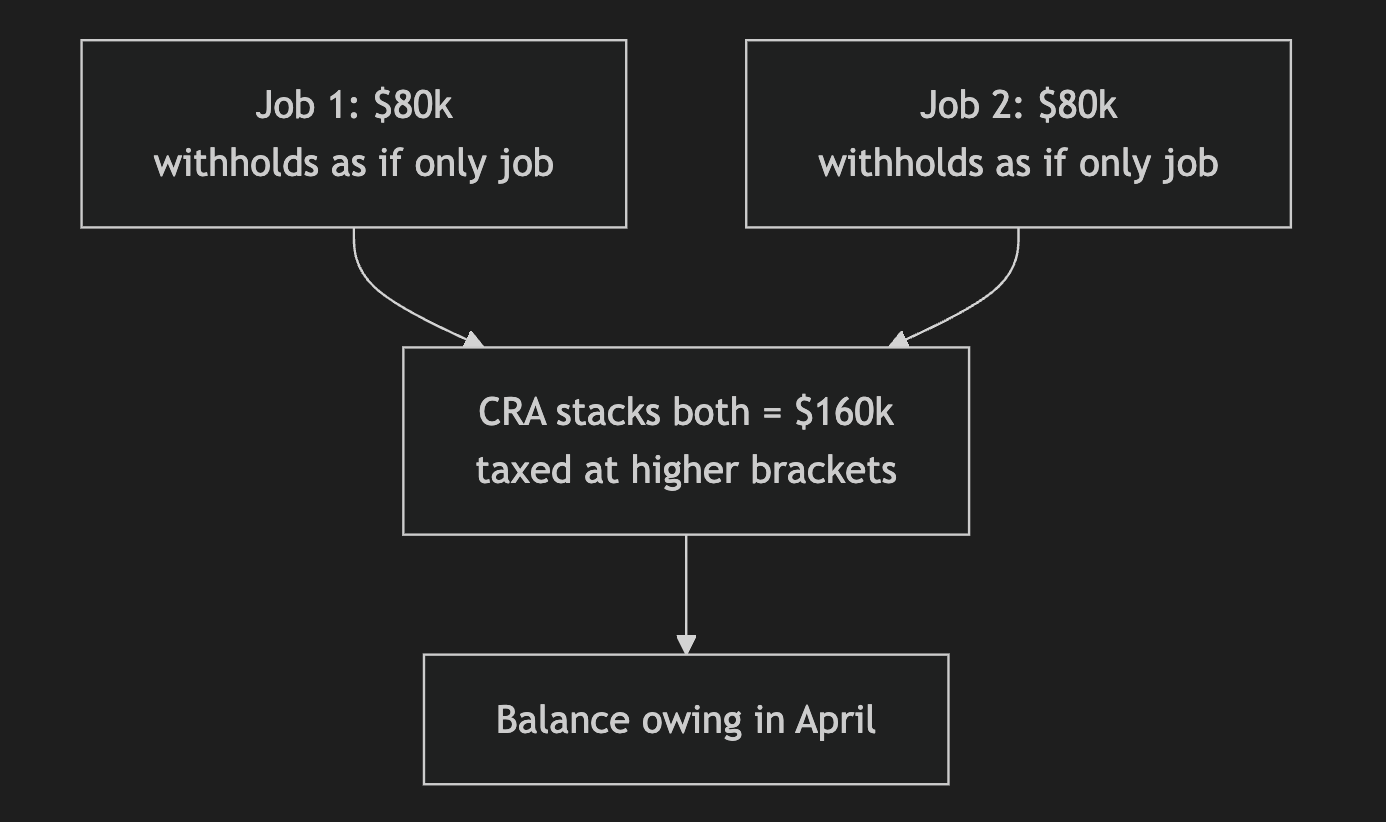

Here is a problem that hits people who hold two jobs at once — two T4s. It is common with remote work, and it surprises people every spring.

Say you have two jobs, each paying $80,000. You think: each one withholds tax, so I am covered. You are not. At tax time you can owe a large balance.

Why? There are two reasons, and they stack.

Reason 1 — the tax-free amount gets counted twice. Each employer’s payroll system bakes in the basic personal amount (~$16,129). Each one treats the first ~$16k it pays you as tax-free. With two jobs, that tax-free chunk is applied twice. But you only get it once. So a big slice of income had no tax withheld against it.

Reason 2 — each job withholds at the wrong bracket. Each employer withholds as if its $80,000 is your only income. So each uses the lower brackets that fit an $80k earner. But the CRA stacks both jobs into $160,000 and taxes the top slice at the higher 26% bracket. Neither employer can see the other, so neither withholds enough on that top slice.

For a data engineer, this is a familiar bug: two systems each compute correctly against local state, but no one holds the global state. The total is wrong until the CRA reconciles at year-end.

The fix. On the TD1 for your second job, tell that employer not to apply the basic personal amount again. You can also ask them to withhold extra tax each paycheque. Or just save the gap yourself and pay it in April — but if the balance gets big, the CRA can make you pay by quarterly instalments next year.

Key takeaways

Two jobs under-withhold for two reasons: doubled tax-free amount and wrong bracket.

Fix it on the second job’s TD1, or save the gap yourself.

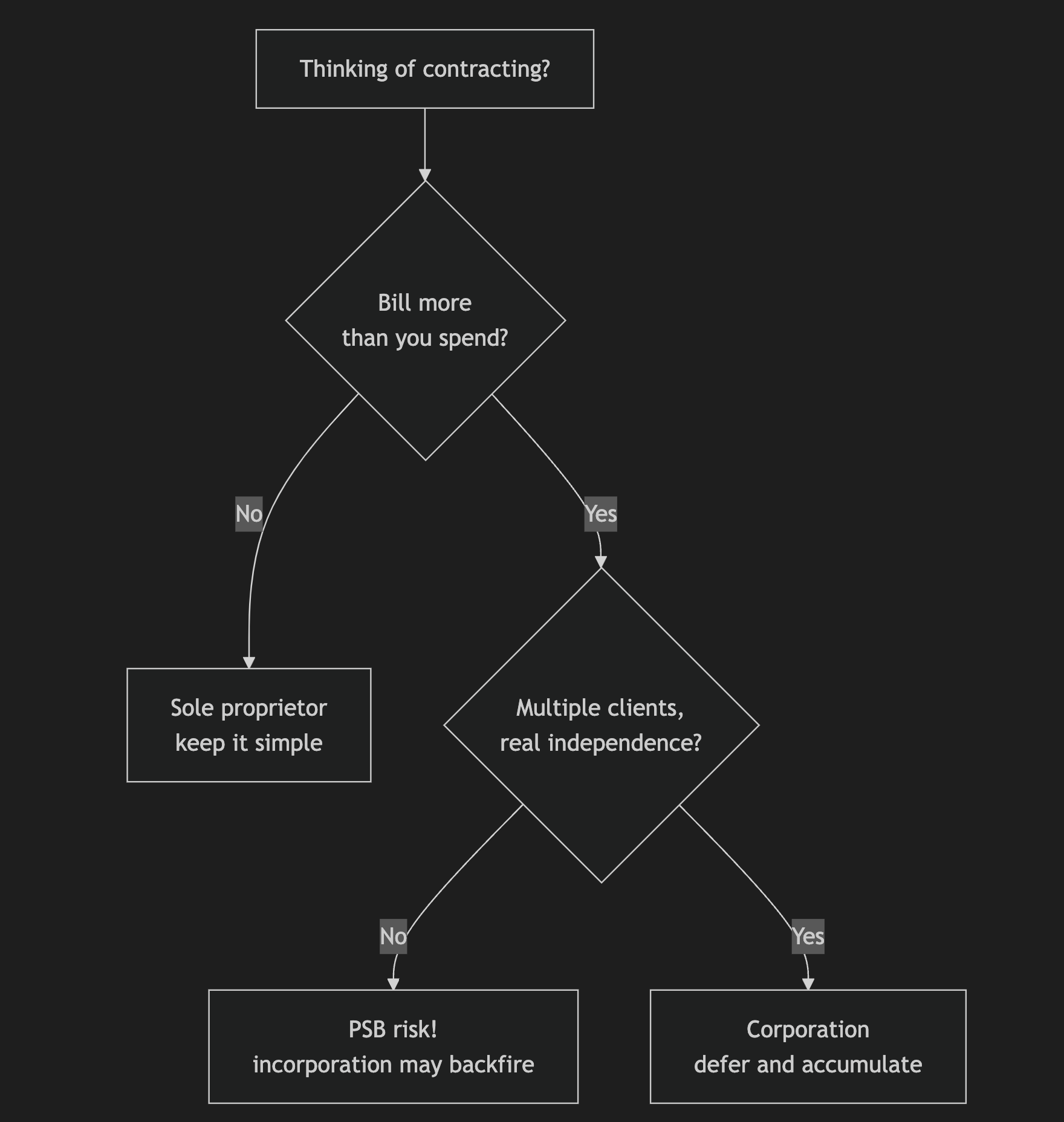

Going independent: sole prop vs corporation

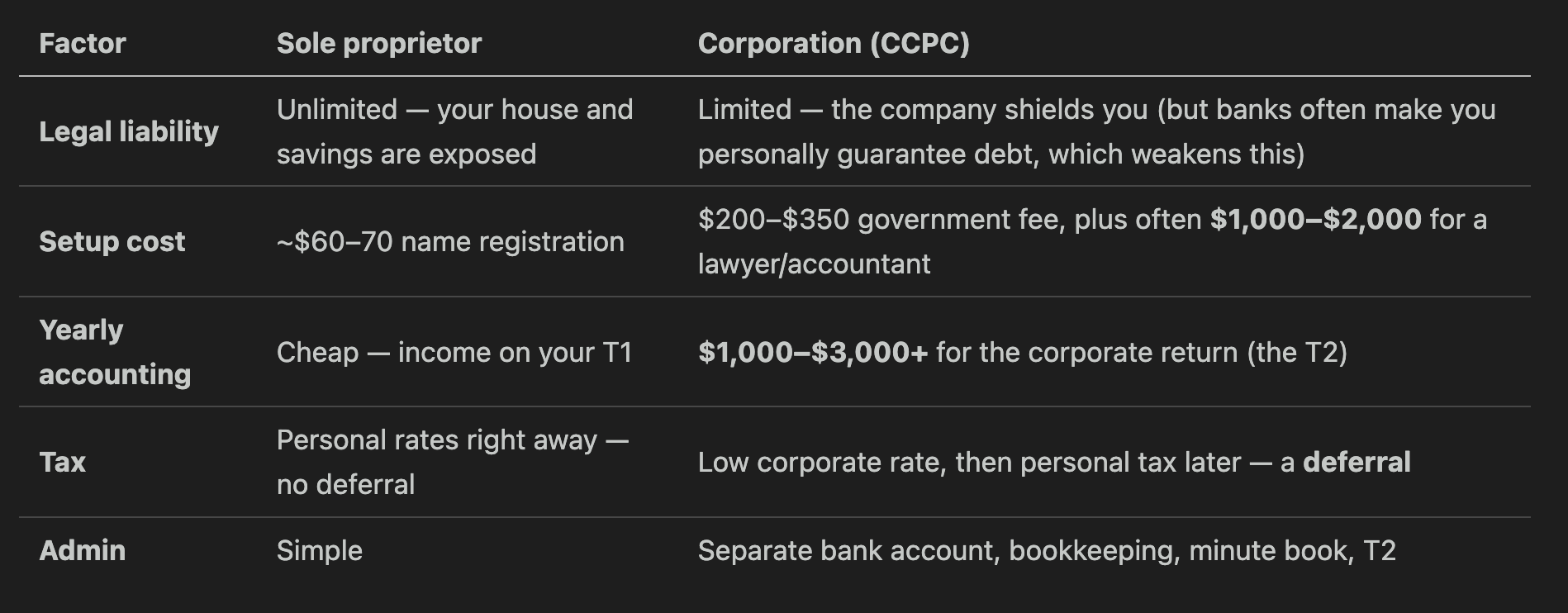

Now we leave employment. As a data engineer you can also work as a contractor. You bill clients instead of drawing a salary. In Canada you can do this two ways: as a sole proprietor or through a corporation.

A sole proprietor is just you, doing business under your own name. No separate company. Your business income goes straight onto your personal tax return.

A corporation is a separate legal entity that you own. In Canada, a small one owned by residents is called a CCPC (Canadian-Controlled Private Corporation). The company earns the money, pays its own tax, and then pays you.

Here is the honest comparison:

The small business deduction

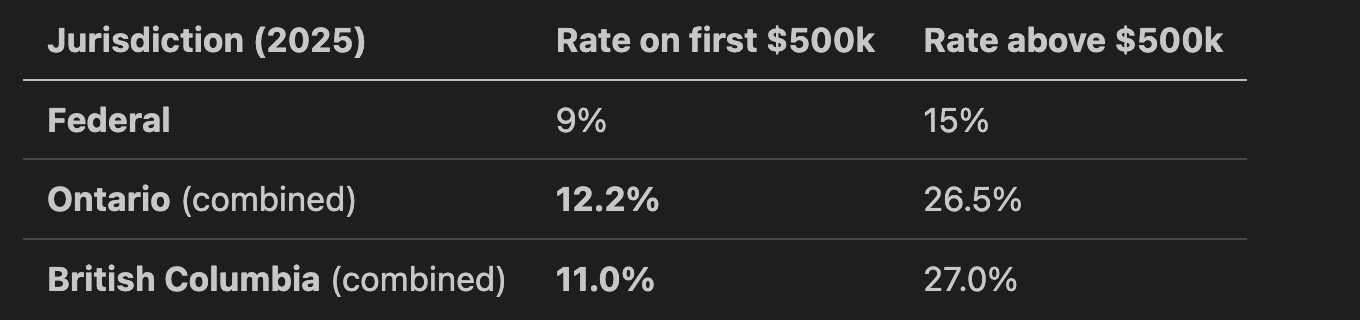

The reason people incorporate is the low corporate tax rate. A CCPC pays a special low rate on its first $500,000 of active business income each year. This is the small business deduction (SBD).

Compare that ~12% to the ~53% top personal rate. That gap is the whole game. But — and this is critical — that gap is a deferral, not a gift. We come back to that later.

When does incorporation make sense?

Incorporate when all of these are true:

You bill far more than you need to live on, so you can leave money in the company.

You want liability protection.

You are not a disguised employee of one client (see the PSB warning).

If you spend everything you earn, incorporation often is not worth it. The $1,500–$3,000 of yearly accounting can eat the small deferral benefit. “Incorporate to save tax” is oversold advice.

Key takeaways

Sole proprietor is simple but offers no liability shield.

A corporation pays ~12% on the first $500k — but that is a deferral.

Only incorporate if you bill more than you spend and you are truly independent.

Running the corporation

Say you incorporated. Now you run the company. Here is what that involves, and where the real traps hide.

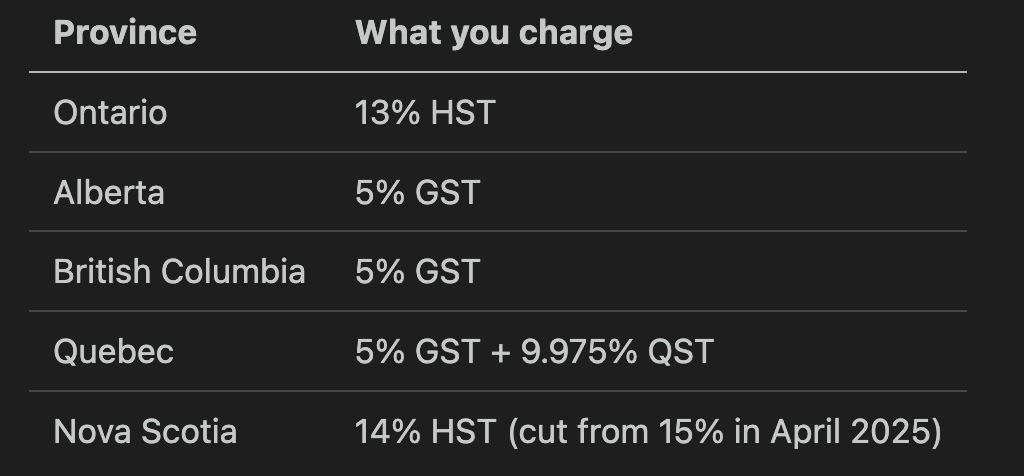

GST/HST — the sales tax you charge

Once your business income passes $30,000 over four rolling quarters, you must register for GST/HST (the federal sales tax). After that you add the tax on top of your fee and pass it to the CRA. You are collecting it for the government, not keeping it.

Example: a $1,000 invoice in Ontario becomes $1,000 + $130 HST = $1,130.

The good news: you get back the GST/HST you pay on business expenses. These are input tax credits (ITCs). You remit only the difference. If your expenses are low, look at the Quick Method, where you remit a flat percentage instead of tracking every credit.

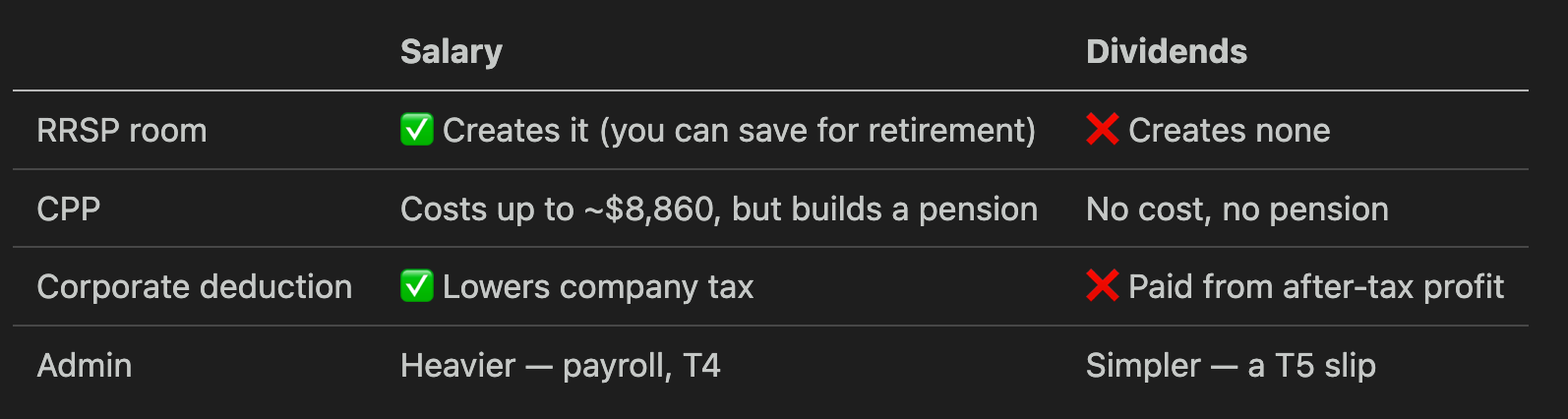

Salary vs dividends — how you pay yourself

Your company has money. How do you move it to your pocket? Two ways: salary or dividends.

The Canadian system is built on integration: the total tax (company plus personal) is roughly the same whichever you pick. The differences are small. A common setup is enough salary to build RRSP room and CPP, then dividends for the rest.

The deferral strategy. Here is the real benefit of a corporation. If you do not need all the money to live on, you leave it in the company. It was taxed at only ~12%, not ~53%. You then invest that larger after-tax sum inside the company. You pay the personal tax later, when you take it out — maybe in a low-income year.

This is powerful. But remember: it is a deferral, not free money. You pay the personal tax eventually. And if you pile up too much passive investment income (over $50,000 a year), it starts to claw back your small business deduction.

Income splitting with family — read this carefully

You may have heard you can “pay your spouse” or “pay dividends to your kids” to split income and lower tax. This was true before 2018. It mostly is not true anymore.

In 2018 the CRA brought in the TOSI rules — Tax on Split Income. TOSI taxes dividends paid to a family member at the top rate unless they pass strict tests. The usual escape (called “excluded shares”) is closed for a data engineering business, because more than 90% of your income comes from services.

So here is the accurate picture:

❌ You cannot pay dividends to a non-working spouse to save tax. It gets taxed at the top rate.

❌ You cannot pay dividends to adult kids who do not work in the business.

✅ You can pay a reasonable salary to a spouse or child for real work they actually do. That salary is deductible. You must document it: a job description, fair market pay, and real hours.

On employing children: there is no minimum tax age, but the work must be real and the pay must match the market. Provincial labour law sets the minimum working age (often around 12–16). Paying a child for work they did not do gets the deduction denied.

⚠️ The biggest trap: Personal Services Business (PSB)

This is the most important warning in this post. If you incorporate but then bill ~full-time to one client, use their laptop, work their hours, and look like one of their staff, the CRA can call you a Personal Services Business — an “incorporated employee.”

The punishment is severe. Your corporate rate jumps from ~12% to about 44.5–45%, and you lose almost all deductions. The whole reason you incorporated disappears.

The CRA actively audited IT consultants for this in 2022–2024. A data engineer billing 40 hours a week to a single client is exactly the profile they look for.

How to stay safe: serve multiple clients, use your own equipment, sign a real contract, control how and when you work, and carry real business risk (fixed-price or milestone work, not pure hourly on one client).

What you can deduct

A corporation can deduct reasonable costs of earning income. Common ones:

Home office — a share of rent, utilities, and internet, based on the space used.

Equipment — laptops and gear (written off over time as Capital Cost Allowance).

Software — your SaaS tools and subscriptions.

Vehicle — the business-use portion, with a logbook.

Professional fees — your accountant and lawyer.

Meals — only 50% deductible.

(Note: if you are deemed a PSB, most of these are denied. Another reason PSB matters.)

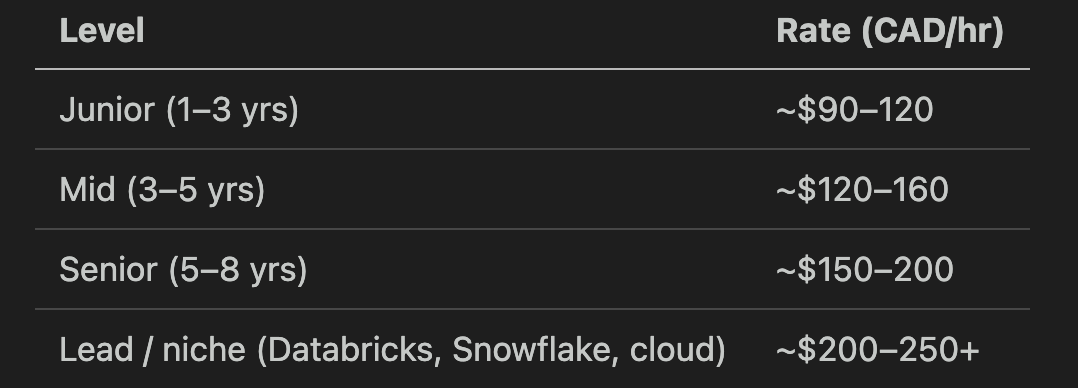

What can you charge? Canadian DE contractor rates

Real independent contractor rates for data engineers in Canada (CAD per hour):

Contractor rates look high next to a salary because you fund your own benefits, vacation, downtime between contracts, and both halves of payroll tax. A $143k mid-level salary is about $70–79/hr as an employee; the contractor markup roughly doubles it.

Key takeaways

Charge GST/HST on top once you pass $30k; claim back ITCs on expenses.

Salary vs dividends is roughly integrated — the real win is deferral.

TOSI killed free dividend-splitting with family; only a reasonable salary for real work survives.

PSB is the #1 risk for a single-client incorporated contractor.

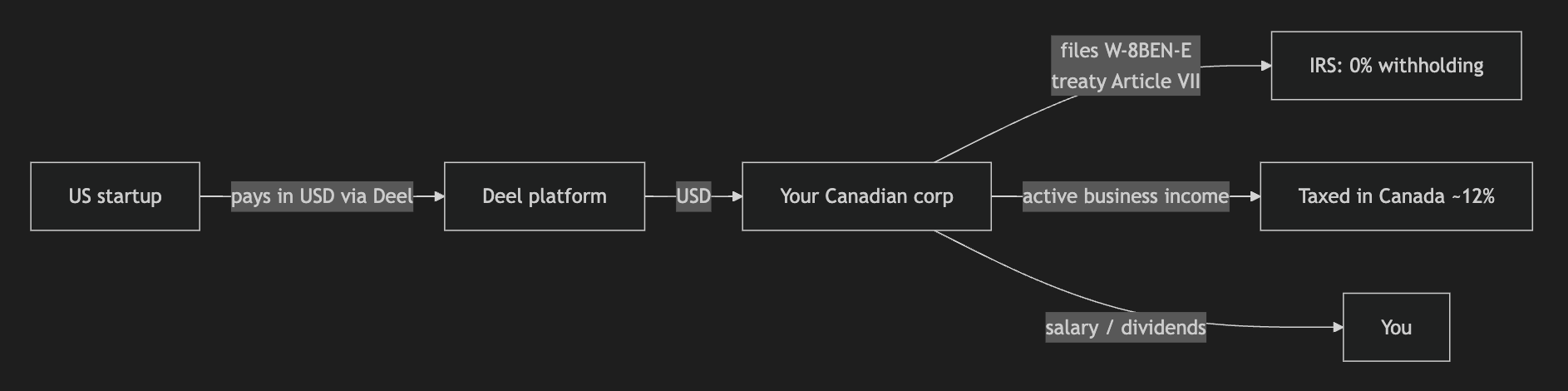

Cross-border: earn USD from a Canadian corp via Deel

Here is a setup that did not exist a decade ago. You live in Canada. You have a Canadian corporation. You invoice a US startup and get paid in US dollars. This is now normal, and platforms make it easy.

Tools like Deel, Remote.com, Oyster, and Rippling let a company hire and pay someone in another country without opening a local office. They come in two flavours:

Employer of Record (EOR) — the platform becomes your legal employer in your country, runs payroll, and handles local tax.

Contractor payment — the platform onboards and pays you as an independent contractor. No tax withheld; you handle your own.

For a Canadian with a corporation, the contractor model is the common one. Here is how the money and the tax work:

The key form is the W-8BEN-E (the entity version of W-8BEN, which is for individuals). Your corporation files it with the US payer. It certifies your company is foreign and claims the Canada–US tax treaty. Under Article VII of that treaty, a Canadian company’s business profits are taxed only in Canada if it has no permanent base in the US. With the form on file, the US payer generally withholds 0%. The income is then taxed in your Canadian corporation at the ~12% small business rate.

The currency upside. In 2025–2026 one US dollar was worth about 1.40 Canadian dollars. So every USD you bill becomes ~$1.40 CAD. You earn in a strong currency and spend in a weaker one. That is a quiet raise on top of your rate.

It works from anywhere. This is not a Canada-only trick. A contractor in almost any country can use Deel-type platforms to work for companies worldwide and hold earnings in USD.

The caveats. Two rules to respect:

Classification. Both the IRS and CRA can reclassify a “contractor” who acts like an employee. Stay genuinely independent — own company, own tools, control your work.

Tax residency. You owe income tax where you live and work, not where the client sits. The platform does not change that.

Key takeaways

A Canadian corp can invoice US clients via Deel and get ~0% US withholding with a W-8BEN-E and the treaty.

You earn USD, spend CAD, and pocket the ~1.40 exchange.

Works globally — but you still pay tax where you live.

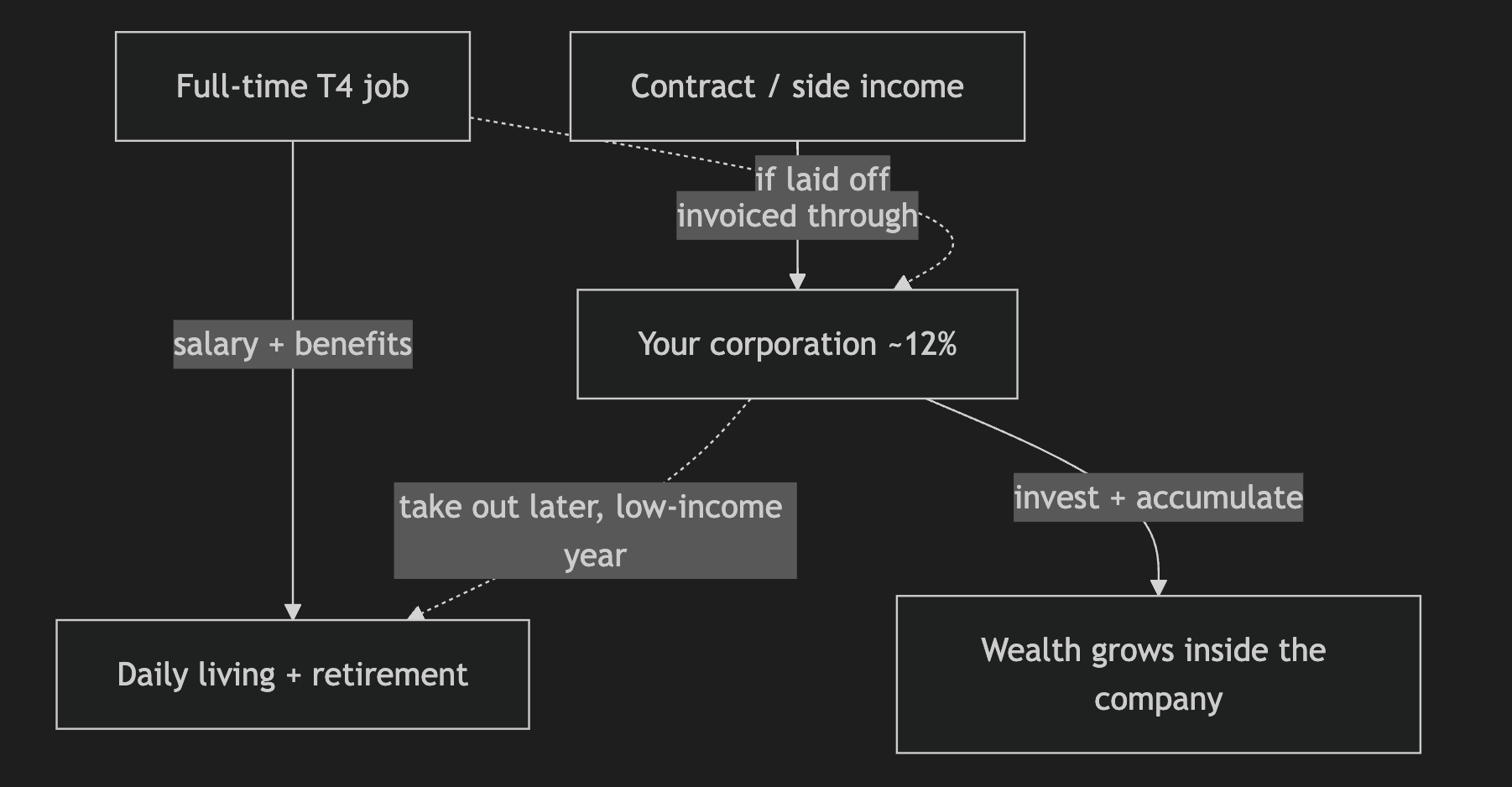

The best setup: keep the T4, run the corporation

Now put it all together. After looking at every option, one combination stands out for many data engineers. It is not the flashiest. It is the most resilient.

Keep a full-time T4 job — and run a corporation on the side.

Each half covers the other’s weakness:

The full-time job gives you:

A steady salary and benefits — health coverage, paid time off.

Stability — a base income that does not vanish between contracts.

Retirement room — RRSP contribution room that a salary builds.

A predictable marginal tax rate you understand.

The corporation gives you:

A place to put contract work, side projects, or any business income.

The low ~12% corporate rate on that extra income.

A way to accumulate and invest money inside the company while you live on your salary.

Room to expense legitimate business costs.

You live off the job’s salary. The side income piles up in the company at the low rate. You invest it there and defer the personal tax until you need it — maybe years later, in a lower-income season or early retirement.

Be honest about the limits:

The PSB line still applies. If your “side” work is really one full-time client wearing a costume, the CRA can treat the corp as a Personal Services Business. Keep the corporation doing genuine, varied business.

It is still a deferral. The corporate money is taxed personally when you take it out. You are smoothing and delaying tax, not escaping it.

It depends on your numbers. This setup shines when you earn more than you spend. If you spend everything, the simpler T4-only path may be better.

Watch your time. Holding a job and a real business is real work. Do not let the side business quietly become a second full-time job with no benefits.

For many mid-to-senior data engineers, though, this is the sweet spot: the safety of employment, plus a tax-efficient engine for everything extra you build.

Make the money work: RRSP, TFSA, RESP, and covered calls

Everything so far was about how money comes in. This part is about where it goes — because Canada gives you three registered accounts that change the tax math again, plus a way to squeeze extra income out of stock you already own.

RRSP — the tax-deferral machine

The RRSP (Registered Retirement Savings Plan) is the pre-tax account. You earn room at 18% of last year’s earned income, up to $32,490 for 2025. (Remember from Part 5: salary creates RRSP room, dividends do not — one more reason to pay yourself at least some salary from a corporation.)

The mechanics are simple and powerful:

Contribute → the amount is deducted from your taxable income. At a senior engineer’s ~53% marginal rate, a $10,000 contribution puts roughly $5,300 back in your pocket at tax time.

Grow → investments inside compound with no tax on gains or dividends.

Withdraw later → taxed as income, ideally in retirement or a low-income year at a much lower rate.

It is the same logic as the corporation in Part 5: defer tax from your ~53% years to your cheap years.

A bonus for stock-heavy portfolios: under the Canada–US treaty, US dividends inside an RRSP are exempt from the 15% US withholding tax. The RRSP is the best home for US dividend payers.

The RRSP can also buy your house. Under the Home Buyers’ Plan (HBP), a first-time buyer can withdraw up to $60,000 from their RRSP tax-free toward a home — $120,000 for a couple — and repay it into the RRSP over 15 years. Combined with the newer FHSA (First Home Savings Account: $8,000/year, $40,000 lifetime, deductible going in and tax-free coming out for a first home), a young data professional has serious tax-advantaged room to build a down payment.

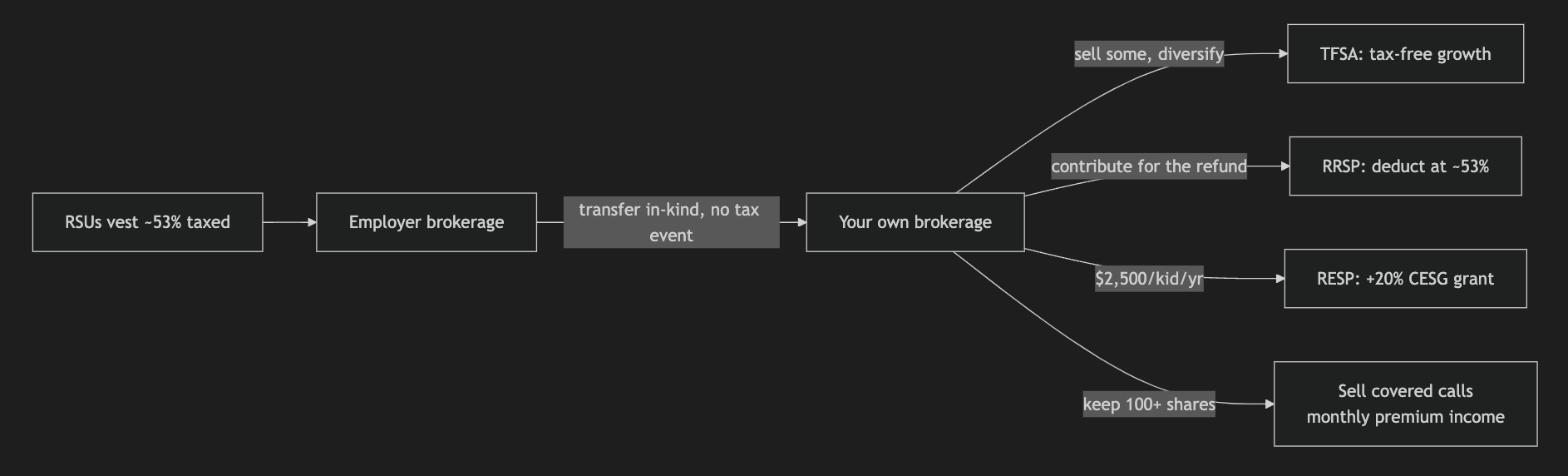

TFSA — the tax-free bucket

The TFSA (Tax-Free Savings Account) is the mirror image. No deduction when money goes in — but zero tax, forever, on everything inside: growth, dividends, withdrawals. Room accrues at $7,000 per year (2025); an adult who has been eligible since 2009 has roughly $102,000 of cumulative room. Whatever you withdraw is added back to your room the following year.

Here is the move for anyone with vesting stock: as RSUs vest, sell some shares, move the cash into your TFSA, and reinvest there. The vesting value was already taxed as income (Part 2) — that tax is sunk either way. But every dollar of future growth inside the TFSA is never taxed again. You also cut your concentration in employer stock at the same time — two wins in one trade.

Two caveats:

US dividends inside a TFSA still lose the 15% US withholding — the treaty does not cover TFSAs. Keep US dividend stocks in the RRSP; keep growth stocks and Canadian holdings in the TFSA.

Do not day-trade it. If the CRA decides you are running a trading business inside a TFSA, the gains become fully taxable business income.

RESP — free money for your kids

If you have children, the RESP (Registered Education Savings Plan) is the closest thing to a guaranteed return in Canadian finance. The government matches your contributions through the CESG (Canada Education Savings Grant): 20% on the first $2,500 per year per child = $500 of free money annually, up to a $7,200 lifetime grant per child. Lifetime contribution cap: $50,000 per child.

That is a 20% instant return before the market does anything. Inside the plan, everything grows tax-deferred. When the money comes out for school, the growth and grants are taxed in the student’s hands — and a student with little income typically pays ~nothing.

The play: contribute $2,500 per kid per year to capture the full grant, invest it, and let 18 years of compounding run.

Covered calls — extra income from stock you already hold

Back to those vested RSUs from Part 2. After vesting, the shares usually sit at the employer’s broker. You can transfer them in-kind (no sale, no tax event) to your own brokerage — Interactive Brokers, Questrade, and others handle this routinely.

Once you hold 100+ shares of the stock in your own account, you can sell covered calls against them: you collect a premium today for agreeing to sell your shares at a higher strike price by a set date.

Stock stays below the strike → the option expires, you keep the premium and the shares, and you can do it again next month.

Stock rises above the strike → your shares are called away — sold at the strike. You keep the premium plus the gain up to the strike, and the sale triggers a capital gain (50% inclusion, Part 2).

On a large vested position, monthly premiums can add a meaningful income stream on top of stock you were holding anyway. For a typical investor, premiums in a taxable account generally get capital-gains treatment.

The honest caveats:

You cap your upside. In a strong rally the shares get called away and you miss the run above the strike. Never sell calls on shares you are not willing to sell at that price.

Company policy still applies. Insider-trading rules, trading windows, and blackout periods usually cover options on your employer’s stock too. Check before you trade.

Concentration is still concentration. Covered-call income is not a reason to stay overweight your employer. Salary, RSUs, and a levered stock position in the same company is a lot of eggs in one basket — a layoff and a stock drop tend to arrive together.

The mortgage bonus: home office

One more link back to deduction list. If you work from home through your corporation or as a self-employed contractor, the business-use share of your home costs is deductible — and with a mortgage that includes the mortgage interest (not the principal), plus property tax, utilities, insurance, and internet, prorated by the office’s share of your home.

Example: a 150 sq ft office in a 1,500 sq ft home = 10% of interest, property tax, and utilities becomes a business expense.

Two boundaries:

Employees can’t claim mortgage interest. On a T2200 employee home-office claim, rent qualifies — mortgage interest and property tax do not. This deduction belongs to the self-employed and incorporated.

Never claim CCA (depreciation) on the house itself. It can poison the principal-residence exemption and make part of your home’s growth taxable when you sell. Every accountant will tell you the same: take the interest share, skip the CCA.

Key takeaways

RRSP: deduct at ~53% now, grow tax-free, withdraw cheap later; US dividends inside avoid the 15% withholding; HBP lends you $60k of it for a first home (plus the FHSA’s $40k).

TFSA: $7,000/year of room; sell vested RSUs, reinvest inside, and the future growth is never taxed — while cutting employer-stock concentration.

RESP: a 20% government match ($500/kid/year, $7,200 lifetime) — capture it every year.

Covered calls on vested shares add premium income — transfer in-kind, mind trading windows, and accept the capped upside.

With a mortgage, the home office deducts the interest share (corp/self-employed only) — but never claim CCA on your house.

Growing bigger: holding companies, multiple corporations, and family trusts

Everything so far fits a solo professional. But suppose the plan works. Your corporation piles up retained earnings, you add a second line of business, maybe you build something you could one day sell. At that scale, Canada offers another tier of structures. This is where the real long-term tax planning lives — and where you stop reading blog posts and start paying professionals. Here is the map anyway.

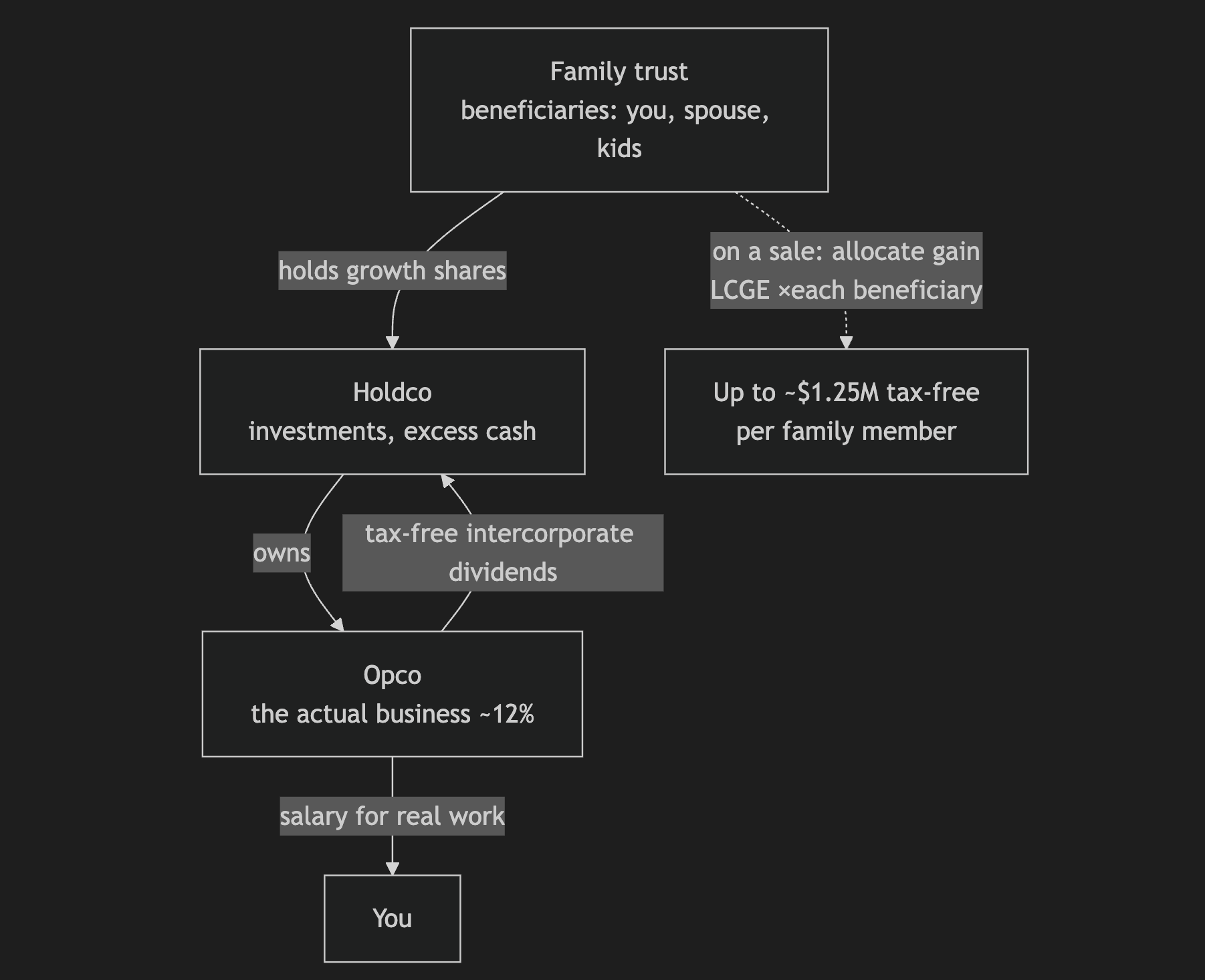

The holding company: Opco + Holdco

The classic first upgrade. You split into two companies:

Opco (operating company) — does the actual work: consulting, contracts, products. Carries all the business risk.

Holdco (holding company) — owns Opco’s shares and does nothing but hold money and investments.

Why bother? Because dividends between connected Canadian corporations flow tax-free. Opco earns at ~12%, pays its excess cash up to Holdco with no extra tax, and Holdco invests it.

Two real benefits:

Creditor protection. Opco faces the world — clients, contracts, lawsuits. If it ever gets sued, the years of accumulated cash are not sitting there as a prize. They are one level up, in Holdco, out of reach. You keep Opco “cash-poor” on purpose.

A clean company to sell. A buyer wants your business, not your investment portfolio. With the portfolio in Holdco, Opco stays a pure, sellable business — which also matters for the capital gains exemption below.

One warning carried over: the $50,000 passive-income limit counts across associated corporations combined. Moving investments to Holdco does not reset it — above $50k of passive income, the group’s small business deduction starts to shrink (it is gone entirely at $150k). Holdco relocates the money; it does not hide it.

Multiple corporations: separation, not multiplication

As you grow, it can make sense to run separate corporations for separate things: the consulting Opco, a company for a SaaS product, a company for a rental property. The point is risk isolation and clean books — if one venture fails or gets sued, the others are untouched, and each can be sold or shut down on its own.

The point is not tax multiplication, and this is the trap people walk into: you might think five corporations mean five × $500,000 of small-business-rate income. They do not. Corporations under common control are associated, and associated corporations share one $500k small business limit. The CRA closed that door decades ago.

So open a second corporation when a business line genuinely needs its own walls — and remember each one adds $1,000–$3,000 a year in accounting and its own filings.

The family trust: the biggest legal win left

A discretionary family trust does not do work and does not earn fees. It holds shares — typically of Holdco or Opco — for a list of beneficiaries: you, your spouse, your kids, often a corporate beneficiary too. The trustees (usually you) decide later who gets what. That flexibility is the tool.

Be clear about what it does not do: TOSI applies through trusts. A trust does not revive sprinkling dividends to a non-working spouse or kids — that door stayed shut in 2018.

What it does do is bigger. Every Canadian has a Lifetime Capital Gains Exemption (LCGE) — about $1.25 million of capital gains, completely tax-free, on the sale of qualified small business corporation (QSBC) shares. One person selling a business uses one exemption. But when a family trust holds the shares, the trustees can allocate the sale gain across the beneficiaries — and each one uses their own exemption.

Family of four, business sells for $5M of gain: allocated through a trust, potentially the entire $5M is tax-free. Without the trust, one exemption shelters $1.25M and the rest is taxed. That single difference can be worth over a million dollars in tax — and it is the reason the trust must exist years before a sale, not the month before.

The supporting act is the estate freeze: you “freeze” the current value of your shares into fixed-value preferred shares, and new common shares — all future growth — are issued to the trust. Your eventual tax bill at death is capped at today’s value; everything the business grows into after belongs to the next generation, with tax deferred until they sell.

The honest fine print

Trusts have a 21-year clock. Every 21 years a trust is deemed to sell everything at fair market value. Plans must deal with that horizon.

Real costs. A trust runs $3,000–$10,000 to set up properly, plus annual T3 filings and legal upkeep. A Holdco adds its own accounting. This tier only pays for itself at real scale.

The QSBC test is strict. For the LCGE, roughly 90% of the company’s assets must be active business assets at sale (and 50%+ for the 24 months before). A corporation stuffed with passive investments fails — one more reason the Holdco/Opco split matters.

When is it worth it? Rough rule: a Holdco starts making sense once retained earnings reach the high six figures; a family trust makes sense when a future sale of the business is plausible or estate planning is in view. A solo contractor billing $150k and spending most of it needs none of this.

Do not DIY. This is the one part of this post where “talk to a professional” is not a disclaimer — it is the instruction. Trusts and freezes done wrong create tax problems instead of solving them.

Key takeaways

Holdco + Opco: tax-free intercorporate dividends move excess cash out of harm’s way and keep the business clean to sell.

Multiple corporations isolate risk — but associated corps share one $500k small business limit. No multiplication.

A family trust multiplies the ~$1.25M lifetime capital gains exemption across family members on a business sale — the biggest legal tax win left, but it must be set up years in advance.

An estate freeze caps your death-tax bill and passes future growth to the next generation.

This tier has real costs and a 21-year clock — it pays off at scale, with professionals, not from a blog post.

Summary

T4 employment is the simple default. The employer withholds tax, CPP, and EI; you get a slip and file once a year.

Tax is marginal. Only the dollars in a higher bracket are taxed more. Top rate is ~53.5% in Ontario/BC.

Two jobs under-withhold for two reasons. Fix it on the second job’s TD1 or save the gap.

Contracting means billing clients — as a sole proprietor (simple) or a corporation (deferral).

A corporation’s tax win is a deferral, not free money — ~12% now, personal tax later.

TOSI killed free family dividend-splitting. Only a reasonable salary for real work survives.

PSB is the biggest trap — a single-client incorporated contractor can lose the whole advantage.

Cross-border via Deel lets a Canadian corp earn USD with ~0% US withholding, taxed in Canada.

The strongest setup for many: keep a full-time job for stability and benefits, and run a corporation for everything extra — because job security is a myth and you build your own.

Put the money in the right buckets: RRSP (deduct at ~53%, HBP lends $60k back for a first home), TFSA (sell vested RSUs, reinvest, never taxed again), RESP (a guaranteed 20% government match for your kids).

Squeeze the stock and the house: transfer vested shares in-kind and sell covered calls for premium income; if self-employed or incorporated, expense the home-office share of your mortgage interest — but never claim CCA on the house.

At scale, upgrade the structure: a Holdco protects accumulated cash and keeps the business sellable; a family trust can multiply the ~$1.25M capital gains exemption across the family on a sale — set up years ahead, with professionals, because associated corporations share one $500k limit and trusts run on a 21-year clock.

One line to remember: the job pays for your life; the corporation builds your wealth — and an hour with a good accountant pays for itself many times over.

General information for the 2025–2026 tax years, not personal tax or legal advice. Rules change and differ by province and situation. Confirm anything load-bearing — especially PSB status and any family-salary planning — with a qualified accountant.